Research Notes: Cardlytics $CDLX (Quantitative #1)

Research Notes: Cardlytics $CDLX (Quantitative #1)

Quantitative notes from researching, investigating, and thinking through Cardlytics.

If you are coming from a direct link for a given update (such as from Twitter), and if you have access to the notes, it will take you directly to the corresponding section with the update. (If mobile, open in the browser not within the Twitter app, but instead where you are logged in to Substack).

If you do not have access yet, upgrade to a paid subscription here:

These are the CDLX Quantitative Research Notes #1. Use the following link to access the:

I frequently send out emails that contain the most recent updates to these notes:

List of the the most recent updates in the CDLX Research Notes

What Are Research Notes?

Research Notes contain information I have collected while researching, investigating, analyzing, and thinking through the business.

This is where I continue to add additional notes, observations, and thoughts.

Some of the notes have never been made, nor will be made, into official posts that are public to read.

Notes are split into Qualitative and Quantitative Research Notes, given I have hit the limit of content that will save in Substack (despite Substack saying there is no limit, which likely reflects the amount of notes stored here).

For more general information on Research Notes, see here.

Research Notes: Cardlytics $CDLX (Quantitative #1)

Subject

Cardlytics ($CDLX)

Quantitative Research Notes #1

Last Updated

Updated as of 5.11.2023

Best Way to Use and Read

I include a table of contents below. Next to each section is a superscript / footnote number. Click the footnote number, and it will take you to the relevant section.

If there are specific items you wish to read about, I suggest Ctrl+F

How to Know When There are New Notes to Read

When I make an update to the Research Notes, I add the date of the change and the name of the section to the “Update Log” below the Table of Contents.

I also started sending out emails that contain the most recent updates to these notes.

List of the the most recent updates in the CDLX Research Notes

Additionally, I tweet out the update on my Twitter.

You will see the latest additions to the thread on your Twitter feed or when you check out my Twitter profile.

Important Twitter Note: The link in the tweet will take you directly to the section with the new update as long as you open the link in a browser where you are logged into Substack (therefore it will not work if you open it within the Twitter mobile app until you open it in the your main browser on mobile. On iOS, you simply need to click out using the Safari button in the bottom right.)

Table of Contents for Notes #1

These are the notes on this page (for the remained of the notes, see Quantitative Research Notes #2 and #3).

Earnings1

Q1 2023 Earnings Call

Notes and Thoughts After the Call

Notes and Thoughts Before the Call

Q4 2022 Earnings Call

Notes and Thoughts After the Call

Notes and Thoughts Before the Call

Q3 2022 Earnings Call

Notes and Thoughts After the Call

Notes and Thoughts Before the Call

Q2 2022 Earnings Call

Notes and Thoughts After the Call

Notes and Thoughts Before the Call

Q1 2022 Earnings Call

Notes and Thoughts After the Call

Notes Before the Call (Possible Management Changes, Third Party Content Providers, BofA, Numbers, Open Banking, Dosh, Bridg, New Ad Server, New Banks)

Q4 2021 Earnings Call

Notes From After the Call

Notes and Thoughts Before Q4 2021 Earnings Call (Thoughts on Possible Results and What Could be Released / Discussed / Announced. IDFA, CDLX, FB, and More)

Q3 2021 Earnings Call

Notes From After the Call

Notes and Thoughts Before Q3 2021 Earnings Call

Market Price / My Buying and Selling

Update Log

5.8.2023, 5.9.2023

Earnings: Q1 2023 Earnings Call: Notes and Thoughts After the Call

(#176) 5.11.2023: Thoughts After Q1 2023 Earnings Call (Part 3)

(#175) 5.9.2023: Thoughts After Q1 2023 Earnings Call (Part 2)

(#174) 5.8.2023: Thoughts After Q1 2023 Earnings Call (Part 1)

4.3.2023, 4.4.2023, 4.5.2023, 4.7.2023, 4.12.2023, 4.17.2023, 4.18.2023, 4.22.2023, 4.23.2023, 4.24.2023, 4.25.2023, 4.27.2023, 5.1.2023, 5.4.2023:

Earnings: Q1 2023 Earnings Call: Notes and Thoughts Before the Call

(#173) 5.4.2023: Final Thoughts Before Today's Earnings Call

(#171) 5.1.2023: First Thoughts on “Update to Bridg Earnout Payments”

(#170) 4.27.2023: Updated VWAP Projections (5 Days Remaining of 20) + Additional Bridg Earnout Payment Possibility

(#169) 4.25.2023: Updated VWAP Projections (7 Days Remaining of 20)

(#168) 4.24.2023: Follow-up Thoughts on the Timing of Q1 Earnings + Announcing the Bridg Resolution

(#167) 4.23.2023: Thoughts on the Timing of Q1 Earnings + Announcing Bridg Resolution

(#166) 4.22.2023: Updated VWAP Projections (9 Days Remaining of 20)

(#165) 4.18.2023: Updated VWAP Projections (12 Days Remaining of 20)

(#164) 4.17.2023: Current VWAP for 2nd Bridg Earnout Payment + VWAP (Stock Prices and Volume) Projections

(#163) 4.12.2023: Potential Stock Price After the Bridg Resolution

(#161) 4.7.2023: Interpreting the Possible Timings of Announcements

(#160) 4.5.2023: 2025 Convertible Senior Notes + Updated Liquidity Analysis / Share Count / Future Value (with 100% cash for 2nd earnout)

(#159) 4.4.2023: Updated Liquidity Analysis / Share Count / Future Value (Based on higher stock price for VWAP + updated guidance)

(#158) 4.3.2023: Dates for 2nd Bridg Earnout Payment VWAP, and Timing of Possible Announcements / Earnings

3.28.2023:

Thoughts on Market Price Over Time / My Actions

3.3.2023, 3.4.2023, 3.5.2023, 3.6.2023, 3.8.2023, 3.9.2023, 3.11.2023, 3.14.2023, 3.15.2023, 3.18.2023, 3.19.2023, 3.23.2023, 3.27.2023

Earnings: Q4 2022 Earnings Call: Notes and Thoughts After the Call

3.27.2023: Possible Upcoming Announcements that Could Increase the Stock Price for the 2nd Bridg Earnout

3.23.2023: Updated Bridg Dispute Thoughts (Offsetting Factors, Change in Probability, MNPI)

3.19.2023: Updated Liquidity Analysis, Future Share Count, Future Value Per Diluted Share

3.18.2023: New LOC Covenants Related to the Bridg Earnouts and the Dispute (Related to Partial Drawdown of Line of Credit)

3.15.2023: Limit from Accounts Receivable (Related to Partial Drawdown of Line of Credit)

3.14.2023: Partial Drawdown of Line of Credit, and Interest on the LOC (Related to Drawdown)

3.11.2023: CDLX’s and Bridg’s Prior Use of SVB, Updated Liquidity Analysis (Under New VWAP + New Possibility)

3.9.2023: Chase and the New User Experience (on the new ad server), Convertible Senior Notes (a change related to maturity)

3.8.2023: Insider Buying, Confirmation of Reporting Mistakes, Confirmation of an Executive Leaving

3.6.2023: Changes to the Line of Credit, Bridg Earnouts and Dispute Updates, Liquidity After Bridg Earnouts and Dispute

3.5.2023: Actual/Guidance vs Expected Financials (MAUs, Billings Margin, Revenue, Gross Profit, EBITDA, FCF)

3.4.2023: Potential Reporting Mistakes (x3): Latest 10-K, Press Release, etc.

3.3.2023: New User Experience, New Ad Server, Product-Level Offers, Category-Level Offers, Engagement Stats, NOLs, Shares Outstanding

2.5.2023

Earnings: Q4 2022 Earnings Call: Notes and Thoughts Before the Call

2.5.2023 #2: Bridg Dispute and Liquidity

2.5.2023 #1: Macro Ad Market, New Offers, New Ad Server, New Banks

11.1.2022, 11.2.2022, 11.10.2022, 11.11.2022, 11.12.2022, 11.16.2022, 11.18.2022, 12.4.2022, 12.5.2022, 12.7.2022

Earnings: Q3 2022 Earnings Call: Notes and Thoughts After the Call

12.7.2022: Dec 7 Raymond James Conference Notes / Thoughts

12.5.2022: Second Bridg Earnout + Upcoming Dec 7 Conference

12.4.2022: Charging for Engagement to "Better Optimize the Monetization"

11.18.2022: Revenue Share (Deferring vs Boosting Offers)

11.16.2022: Chase Offers Section Updates

11.12.2022: Increasing Pricing as one method to "Better Optimize the Monetization" (Near-Term Impact / Solution)

11.11.2022: Incorrect Cash Burn Assumptions/Concerns (Related to Macro / Lower Advertising Spend)

11.10.2022: Liquidity / Line of Credit / Bridg Dilution

10.20.2022, 10.25.2022, 10.27.2022

Earnings: Q3 2022 Earnings Call: Notes and Thoughts Before the Call

10.27.2022 - Cost Cutting: Closing Multiple Offices

10.27.2022 - Cost Cutting: Employee Headcount

10.25.2022: Insider Actions, Chase/Figg , Gain/Loss of Bank Partners

10.20.2022: Notes from “How Marketers are Achieving Measurement Confidence in a Time of Performance Pressure”

10.16.2022

Market Price: Thoughts on Market Price Over Time

9.20.2022, and 9.25.2022 x2

Earnings: Q3 2022 Earnings Call: Notes and Thoughts Before the Call

9.25.2022: Detail on layoffs, and employee comments on new CEO

9.25.2022: Current Observation of Actions by Advertisers During this Environment

9.20.2022: Chase updates (related to the new ad server)

9.6.2022 - 9.7.2022

Earnings: Q2 2022 Earnings Call: Notes and Thoughts After the Call

9.6.2022: Later in the day I added to this update, with an additional important observation related to new ad server and Chase migration

9.7.2022: Another update confirming which bank is scheduled to launch the new ad server in Q4 2022.

8.2.2022 - 8.3.2022

Earnings: Q2 2022 Earnings Call: Notes and Thoughts After the Call

7.29.2022

Earnings: Q2 2022 Earnings Call: Notes and Thoughts Before the Call

7.17.2022

Market Price: Thoughts on Market Price Over Time

7.16.2022

Earnings: Q2 2022 Earnings Call: Notes and Thoughts Before the Call

5.6.2022

Market Price: Thoughts on Market Price Over Time

Earnings: Q1 2022 Earnings Call: Notes and Thoughts After the Call

5.2.2022

Earnings: Q1 2022 Earnings Call: Notes and Thoughts After the Call

4.26.2022

Earnings: Q1 2022 Earnings Call: Notes Before the Call

Numbers

Management Changes

BofA Renewal

4.24.2022

Earnings: Q1 2022 Earnings Call: Notes Before the Call

Management Changes

4.22.2022

Earnings: Q1 2022 Earnings Call: Notes Before the Call

Numbers

Management Changes

Market Price: Thoughts on Market Price Over Time

4.20.2022

Earnings: Q1 2022 Earnings Call: Notes Before the Call

Management Changes

4.18.2022

Earnings: Q1 2022 Earnings Call: Notes Before the Call:

Possible Management Changes, Third Party Content Providers, BofA, Numbers, Open Banking, Dosh, Bridg, New Ad Server, New Banks

3.11.2022

Q4 2021 Earnings Notes From After the Call

3.8.2022

Q4 2021 Earnings Notes From After the Call

3.2.2022

Q4 2021 Earnings Notes From After the Call

2.25.2022 - 2.28.2022

Earnings. My Notes and Thoughts Before Q4 2021 Earnings Call. Thoughts on Possible Results and What Could be Released / Discussed / Announced

2.9.2022

Earnings. My Notes and Thoughts Before Q4 2021 Earnings Call. Thoughts on Possible Results and What Could be Released / Discussed / Announced

2.8.2022:

Sentiment by Other Investors Over Time

Thoughts on Market Price Over Time

2.6.2022

Earning. My Notes and Thoughts Before Q4 2021 Earnings Call. IDFA, CDLX, FB, and More

11.2.2021

Q3 2021 Earnings Call

10.12.2021

Sentiment by Other Investors Over Time

10.10.2021

My Notes and Thoughts Before Q3 Earnings Call

10.4.2021

Thoughts on Market Price Over Time

8.6.2021

Thoughts on Market Price Over Time

5.17.2021

Thoughts on Market Price Over Time

5.10.2021

Sentiment by Other Investors Over Time

Disclaimer for Research Notes

There may be incorrect information, outdated information, or errors in the following contents, as the following are notes that I wrote down while researching. I include dates where I have them, making it easier to know when the notes / thoughts were written down. The older the notes, the more likely I have changed my mind or found new information.

This is not investment advice.

This is for educational / informational purposes only.

Please see the Disclaimer page for more details.

**Please Do Not Copy or Share to Non-Paid Subscribers**

I have worked hard to research, analyze, think through, collect, and organize all of these notes. Therefore, please do not copy or share the notes contained in these Research Notes to non-paid subscribers.

If you know someone interested, feel free to add them to a group subscription, gift a subscription, or share directly from this post to give them the option to become a paid subscriber to gain access to these notes.

Thank you for your help and support.

Reviews on the Research Notes

Gain Access

If would like access all these “Research Notes”, upgrade your subscription here:

For more general information on Research Notes, see here.

Earnings: Thoughts Before and After Calls

Q1 2023 Earnings: Notes and Thoughts Before the Call

(#176) 5.11.2023: Thoughts After Q1 2023 Earnings Call (Part 3)

11. Updated FCF Timing Expectations (and an additional liquidity scenario)

In my quick liquidity analysis in Update #174, I assumed $13M of cash burn in Q2, Q3, and Q4, to account for the deferral of CF positive. Assuming CF by Q1 of 2024, this analysis showed CDLX would be fine from the perspective of not needing any additional cash in the near term for operations.

After the call, CDLX has made it seem they are expecting CF positive in 23Q4 given it is a strong quarter due to seasonality, and could still be CF positive in 24Q1 but it may be close given it is a seasonal low, with expectations of CF positive from 24Q2 and forward.

As a second scenario, more closely matching CDLX’s post-call commentary:

$139.2M Q1 Cash Position

- $72.6M Bridg Earnout

- $13M Q2 Burn (mid-point of EBITDA guidance at -$8M, but then used $5M lower for FCF)

- $6.5M Q3 Burn (mid-point of Q2 loss and Q4 breakeven)

- $0M Q4 Burn (seasonal high to get to breakeven)

- $6.5M Q1 Burn (same as Q3, due to seasonal low)

= $40.6M Estimated Ending Liquidity at 3/31/2024

Given less cash burn in this scenario, it leads to higher ending liquidity, and the same conclusion is reached, with CDLX having enough liquidity for operations (thanks to the favorable Bridg outcome).

CDLX also later said they still have some room to cut expenses if needed. I’ve been assuming $45M operating expenses per quarter (based on CDLX in Q4 saying $42M cash cash operating expenses but increasing for merit and promotions), but sounds like CDLX could get that down to maybe $38M. I believe the marco would have to turn quite bad for that to be needed and to occur, but it is an option.

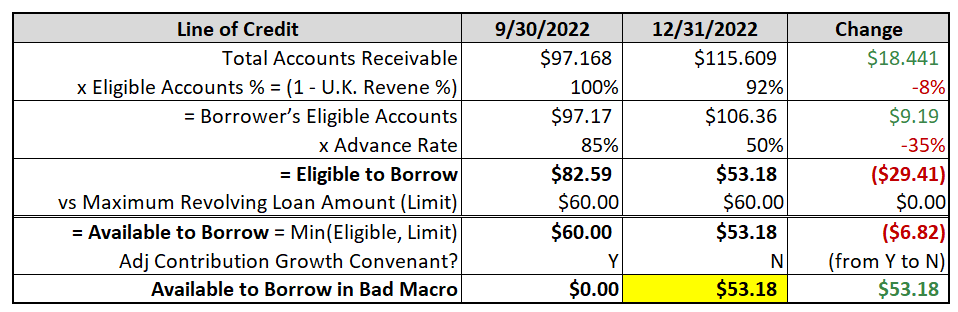

12. Additional Notes on Line of Credit (Amount Available, vs Factoring)

CDLX reported they had $42.282M and $5.48M left on their line of credit, in Q4 and Q1 respectively:

In the 10-Q it says: On November 29, 2022, we amended our 2018 Loan Facility to modify the eligible account receivable to exclude UK accounts, reduce the ability to borrow up to 85% of the amount of our eligible accounts receivable to 50% and adjusted the required minimum level of adjusted contribution.

Using the information CDLX provides + this detail, I get the following when attempting to match their numbers:

12/31/2022: $115.6M account receivable x ~92% US (to exclude UK) x 50% advance rate (used to be 85%) - $0 drawdown as of 12/31 = $53.180M available.

vs $42.282M CDLX lists in the 10-Q (or a $10.898M difference)

3/31/2023: $93.7M account receivable x ~95% US (to exclude UK which is smaller now) x 50% advance rate - $30M drawdown = $14.511M available.

vs $5.48M CDLX lists in the 10-Q (or a $9.031M difference)

I am not quite sure why I am off by $9M-$11M. It could be that UK accounts receivable are a higher percentage than their percentage of revenue. Maybe it is more a function of minimum liquidity requirements. Regardless, this is now much less of a concern given the Bridg outcome and CDLX having enough liquidity for operations.

CDLX did say there are undisclosed calculations based on receivables that leads to the $5.480M at 3/31/2023. While that may be the case, I am still hesitant to believe that, since at one point CDLX said they didn’t disclose any of the LOC information, despite them including every document and amendment in the exhibits at the end of the financial statements (although key figures were redacted). And even here, CDLX provides general information, such as saying UK receivables are excluded and the advance rate decreased to 50%. Again, while this may not matter, if CDLX has more liquidity than they realize, that would be good for them and others to know. And while 99% of the time I would never question a company’s reported numbers, CDLX had many issues in the last report (including even this amount available) + the large error in ARR for Bridg, so I don’t think it is too unreasonable for me to question it. I’m most likely wrong here though. But again, it most likely doesn’t matter, since CDLX has enough liquidity without this additional capacity.

With respect to getting more liquidity with the same accounts receivable, or refinancing the LOC before maturity, CDLX currently says they have no plans to do factoring at this time. However, I believe this could change under the new CFO, given it would seem factoring would lead to more liquidity on the same accounts receivable.

13. Additional Notes on Converts (and potential near-term ARPU)

Wayfair announced yesterday the pricing of $600M converts at 3.5% due 2028. They intend to use the proceeds to repurchase their 2024 and 2025 notes.

While different situations / businesses / balance sheets, to me this is a good sign that CDLX could do something similar in this market with their current 2025 converts. I am not talking about the same terms, but more regarding the fact new converts are occurring in this market.

Many seem to think CDLX will need come up with cash for the 2025 maturity, such as cash from operations, but given what I’ve heard from others + what I’m seeing in the current market, I believe we will see CDLX rollover the existing converts into new ones.

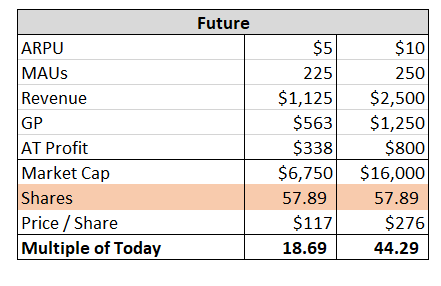

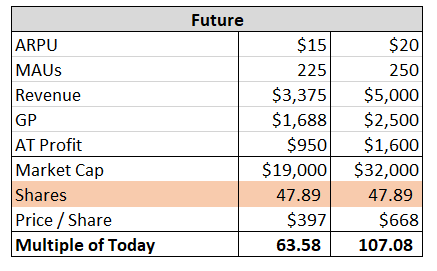

I do not think CDLX will rollover to new converts any time soon, and no reason to do it soon, since have 2+ years. If CDLX executes on their stated plans, it should lead to higher ARPU and CF, which should lead to a higher market price, which likely increases the market price on the converts and decreasing their yield, altogether making any future actions easier.

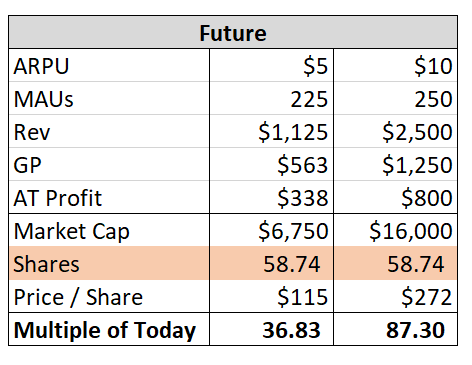

The following is how I’m thinking about potential ARPU in the near to medium term (which should help with the stock price):

I do think CDLX increases ARPU here in the next couple of years, which will have an impact given the large MAU base + operating leverage + near CF positive.

So if they get all banks on new ad server and new user experience by end of this year 2023, then have a full year of new offer constructs like product level offers + more A/B testing + more users seeing and engaging throughout 2024, I think you get to $3-5 ARPU run rate in 2025.

BofA was $2.30 in 2018 with less offers, old tech, old UI, no new offer constructs, etc. ARPU decreased somewhat from denominator effect of large increase in MAUs from Chase and Wells, leading to about the $1.5 seen today.

So should get back to $2.30, then $3 with this now larger reach and additional time and more advertisers, then $4 - $5 with all the other improvements and higher engagement + unlocking new ad budgets through category and product level.

$4 - $5 ARPU is still quite low in relation to Pinterest at $24 TTM for US and Canada, and Snapchat at $31 TTM for US and Canada (I don’t think it is accurate to compare to global ARPU numbers).

(At $5 ARPU run rate x 200M MAUs x 50% rev share - $180M OpEx - $25m delivery costs - $50M extra OpEx and delivery costs for growth) = $245M. (Likely little to no taxes from large NOLs.)

So with a little CF positive in 2024 + this in 2025, could have a small build up of CF that gets close to covering converts.

This requires very good execution by CDLX. But this is also about 2.5 years post Karim taking over, leading to $1B in rev, where at Google in 2.5 years he took the new Global Mobile division from $0 to $10B.

So I don’t think this is crazy, given Karim has more experience now, leveraging existing CDLX infrastructure, essentially only doubling 2018 BofA ARPU from larger reach + new user experience + product-level offers and more, etc.

14. Other Less-Discussed Liquidity Resources

As shown in the liquidity analysis, given the favorable resolution of the Bridg dispute, CDLX likely has enough liquidity even with CF+ being pushed out.

And if things got tight, as also mentioned earlier, CDLX could cut some expenses, or instead securitize / factor their accounts receivable to get more than using it as collateral for the LOC (current CFO will not pursue this, but the new one might).

But there is even another underdiscussed liquidity resource. It isn’t too liquid, but it could be converted to cash if CDLX needed another quarter or two of runway (without taking on additional debt or dilution). I discussed this here, but copied this section of notes for convenience, and updated it to reflect the current situation:

Entertainment as a Liquidity Resource

With CDLX updating the Entertainment app, it got me thinking.

Entertainment could be sold if CDLX really needed the additional liquidity.

Maybe it is harder in this environment to sell, and could come with an even lower price if the buyer knew CDLX was selling out of desperation, but it could be an option.

Entertainment was bought at $14.6M on January 7, 2022 for less than 2x revenue, so approximately $7M in revenue.

With an updated app to improve the product, as well as possible other enhancements learned from CDLX and Dosh, maybe CDLX could still get 2x revenue (meaning, 2x originally, then <2x from environment and force selling, then 2x from improvements).

Where CDLX could likely even get a slightly higher multiple than where they paid, and why this could be a good transaction, is CDLX could agree to still partner with Entertainment to use their offers within the banks. (This is similar in a way to a sale leaseback)

Originally this was one of the purposes of Entertainment, to have this small to mid-market offers within the banking channel.

“Our plan is to use Entertainment's content on the Cardlytics platform once our bank partners launch our new ad server and roll out the new user experience.” - 21Q4 Earnings

If CDLX did use Entertainment offers within the banks, such as under its own tab on the new UI, it would increase Entertainment’s exposure and usage significantly, even if it is just Chase currently. This would increase its value compared to pre-CDLX.

So together you have improving app and features + possibly higher distribution, which could more than offset any multiple contraction in this environment or from a quick sale, and possibly a higher multiple given the expected growth from more banks moving to the new user experience. Then additionally, possibly more subs and higher revenue, leading to both a multiple expansion on top of earnings growth.

In terms of Entertainment having even higher revenue now, there was the trial with AmEx, and CDLX had 40% off offers in all the banks for an Entertainment subscription, so both could have led to more subscriptions and higher revenue.

In terms of estimated revenue:

“For the year ended December 31, 2022, Entertainment's combined revenue included in the consolidated statement of operations was approximately 3% of consolidated revenue, respectively.”

At 3% if $298M of revenue, that is about $9M revenue, showing the growth discussed. 3x multiple is $27M. 4x multiple is $36M. Pretty significant in relation to cash burn around $5M-$15M.

However, it is possible having these offers in the bank is no longer the plan (which would be another reason to sell). Karim mentioned before they are waiting on local offers, or at least with self service for small business. But some of Entertainments offers are mid market, and likely larger than a very small business that has a higher risk of going out of business after placing an offer (which was kind of the risk Karim mentioned from what I remember).

Altogether, it would seem CDLX has more options that one may first think when considering their liquidity options (beyond raising equity, rev share deferral or exchanges for equity, new debt given they are about CF positive, etc.)

Entertainment as a Liquidity Resource (Potential Buyers)

I have been thinking more about the potential divesting of Entertainment to get additional liquidity IF CDLX absolutely needed it, such as if they were not getting to FCF positive.

In terms of who could actually buy Entertainment, and why this may make even more sense than I originally considered, is CDLX could sell Entertainment to one of their bank partners, like Chase. So instead of CDLX getting new financing from someone like Chase, they instead sell Entertainment.

Why I think this could make a lot of sense:

Chase would be helping CDLX stay alive via this cash, which also helps Chase by continuing to have CDLX offers. This may also lead to a more favorable exit multiple. (Some think Chase would want CDLX to fail to buy them up cheap, but the advantage of CDLX is an in independent party who aggregates the banks’ reach).

Chase can then offer Entertainment subscriptions for free to its users. This would be a similar perk to have a free DoorDash subscription or Instacart+, both of which I use with my Chase card.

Chase could also add their SMB clients to the Entertainment app, helping their SMB clients grow their business.

Doing it this way, where maybe Chase does not use these Entertainment offers in their Chase Offers section, it does not create a conflict of interest between the other CDLX bank partners (where Chase would not have further differentiation utilizing these offers that were supposed to be in all banks on the new user experience).

But maybe there is still too much conflict that CDLX cannot sell to a CDLX bank partner. So a very logical buyer is a non-CDLX bank partner who also already trialed offering free Entertainment subscriptions to their users, and continued to offer it as of 3/25…AmEx.

Again, this is only if CDLX absolutely needed the funding. But shows there are options, and CDLX is likely in a better position than most realize.

15. Possible Reasons for Lack of Positive Commentary on the Call

While a lot of the big positive news came ahead of earnings, such as the updated guidance + Bridg resolution, I still felt there was a lack of positive commentary. My first reaction after the call was while there were a few good updates, such as the 50% higher impressions or 74% higher redemptions, there wasn’t too much else.

However, there were signs that CDLX is holding back some of that more positive commentary + updates.

For one, CDLX said after mentioning the 50% higher impressions on the new UI,

“We believe this is only the beginning. As the new UI has rolled out, we've observed other engagement metrics on the new UI that are equally promising, and we intend to disclose some of these statistics when we have scaled data across more bank partners”

Therefore, CDLX wasn’t sharing everything.

So while CDLX has less incentive to provide more positive updates and commentary, I still felt it was strange they wouldn’t want to share more, such as these additional stats.

Well post call, CDLX said too many are focused on liquidity and cash flow at this time, that they did not want to waste providing the other positive items, since they would simply go ignored. Maybe this is not fully the truth, however, it does make some sense, since CDLX would not get credit or market price benefit from sharing non-material positive news at this time. I wonder though if that means CDLX is waiting on holding an investor day.

16. UK Bank Update + Fintechs

In Update #175 I discussed the UK bank that left, Santander, and for Tenerity. Supposedly Santander has already ben disappointed by the switch. So we will see. Could be interesting if they resign with Santander, and with the change in auto enroll, it could end up being a positive, given auto enroll is only for new users, not existing.

CDLX also mentioned the signing of a UK fintech. The only two I really know are Monzo and Revolut, and it sounds like it may end up being one of them. Signing one of these may offset the loss of Santander.

17. Final Thoughts

While cash flow positive is pushed back, this is much less of a concern now given the Bridg resolution, with CDLX having enough liquidity until cash flow positive.

If CDLX absolutely needed additional liquidity before cash flow positive, there are other solutions, such as factoring their accounts receivable to get more than their LOC, or even selling Entertainment, or other options such as a small rights offering (but not too much, to avoid too much dilution at these prices).

Other upcoming liquidity / cash requirements, such as with the maturing of the LOC and 2025 converts, while both something CDLX will need to handle, they are not too much of concern, at least not at this time and not in relation to how much others are worrying about them. There are multiple options to handle both (LOC: extend with PacWest, refi with new bank, factoring AR, etc. Converts: rollover to new converts, other options previously discussed including above), and the ease of handing increases as long as CDLX executes (which is the most important). I do not think we will see these addressed until a new CFO comes in, which will likely be for the better anyway.

So if CDLX can survive the short-term, then the question becomes more a function of the long-term potential value of CDLX.

I still find CDLX trading far too cheap in relation to the medium-term future (let alone the long term), and I don’t think much, if not anything, that was on the call changes that future for CDLX. The loss of the UK bank isn’t great, but CDLX doesn’t need international growth for this to work from an investment perspective at these market prices. And the small early stats with the new user experience is pointing to it having a positive impact.

Stepping back, overall it seems the business is continuing to improve, which increases the odds of realizing the long-term potential of the business:

New CEO, COO, CPO, CTO and soon CFO

Banks are moving to the new ad server, with Chase already on it

Banks plan to rollout the new user experience this year, with Chase already rolling it out (with early stats showing higher engagement)

New offer constructs will be coming out this year, including product-level offers (which have also shown early stats showing improvements)

More US banks are likely to join given ongoing discussions, which will lead to higher MAUs and more reach for advertisers (increasing number of offers, which increases engagement and redemptions by users, leading to more interest from banks and fintechs and so on)

I also think we will start seeing accelerated improvements, with Karim having more time to focus on the business now with the Bridg dispute behind him.

(#175) 5.9.2023: Thoughts After Q1 2023 Earnings Call (Part 2)

The following is the second set of notes and thoughts regarding the Q1 earnings call and 10-Q.

7. Loss of a UK Bank

Geographically, U.S. revenue decreased 0.9% year-over-year. U.K. revenue, which comprises approximately 5% of total revenue, decreased 48.2% in U.S. dollars.

The decrease in U.K. revenue is primarily due to the loss of a bank partner in the channel.

It sounds like the UK bank that CDLX lost is Santander.

It also sounds like this has been known for a while (discussed more below), which could also be why Karim has been so vocal about prioritizing the relationships with the banks.

This loss is not great to hear, but it doesn’t surprise me, compared to if it was a US bank. The reasons this doesn’t surprise me:

It has seemed like the UK division was deprioritized lately, especially after budget cuts. At one point I heard CDLX was shifting resources in the UK to focus on the new ad server.

Peter Gleason, the President of International Operations who was in the UK office left in August 2022 + other senior staff in the UK office. I think the timing was around when there were some layoffs to cut back on expenses.

Additionally, CDLX even said in the past they didn’t have enough scale in the UK for advertisers. Demand is/was there, just not enough reach to take advantage. This was one reason for pursuing open banking. Part of the lack of scale came from not having enough of the major banks, but also due to the opt in requirement for UK users, further limiting the number of UK MAUs, leading to not enough scale (this was CDLX’s issue when they only really had BofA, and changed once they signed Chase and Wells Fargo).

Therefore, between previously lack of prioritizing the banks in general (something Karim has focused on more now) + possible deprioritization or shift in focus + departure of senior staff + not great offers from lack of scale, I can see why this may have occurred.

Given partially a function of past management, and given not a US bank, I am not as concerned.

In terms of the surrounding details of the UK bank that left, there are quite a bit of information online showing Santander is the bank (h/t Poppy for finding all of this).

One article says:

One week left before Santander axes retailer offers: What you need to know

Santander will shut down its current retailer offers scheme next week as it looks to launch ‘Santander Boosts’ – an improved rewards programme.

Retailer offers will be withdrawn a week from today (Thursday 17 November 2022).

This means you will no longer be able to activate deals after this date. But you can activate as many offers before then and they will then be valid for the specific time as per the individual retailer’s terms and conditions, though no later than 31 December.

This confirms CDLX knowing about this for quite a while, given the program ended Nov 17, 2022. The reason CDLX didn’t mention it until Q1 2023, is the program was still active until December 31st.

They also advertised that Santander Boosts will have “even more offeres than you did with Retailer Offers”. And there were discussions that it would have updated imagery and layouts.

In terms of who is powering this new “Santander Boosts”, there was a press release:

Tenerity launches new digital rewards program for Santander.

Tenerity’s Connect platform is the power behind Santander Boosts.

Where “Tenerity operates in 18 countries and our 1400 associates work with more than 2000 clients.” LinkedIn shows 577 employees, so a decent sized company.

More interesting, Tenerity is from cxLoyalty.

Why this is interesting, is in Dec 2020 Chase bought their global loyalty division (source 1 and 2), and not the customer engagement division (now called Tenerity).

cxLoyalty Group Holdings, Inc. ("cxLoyalty Group Holdings") today announced that it has entered into a definitive agreement to sell its Global Loyalty division ("cxLoyalty") to JPMorgan Chase & Co. (NYSE: JPM) ("JPMC"). The deal includes cxLoyalty's leading technology platforms, full service travel agency, gift card, merchandise, and points bank businesses. cxLoyalty will operate as a business unit within JPMC. The transaction excludes cxLoyalty Group Holdings' Global Customer Engagement division and other ongoing businesses (collectively "the Global Customer Engagement Division").

So Chase likely had the opportunity to also buy Tenerity if they wanted to have an in-house offers platform, but did not. (Further indication of Chase intention of staying with CDLX is now seen with them moving to the new ad server + rolling out the new user experience, even nearly 1 year after acquiring Figg, which they said was for SMBs, which CDLX is no longer focused on).

8. New Banks and Fintechs

There are several new initiatives that we expect to increase our MAU base, including an enhancement by one of our large U.K. partners that will result in users being auto enrolled into our program and the launch of new bank partners that we expect to occur in late 2023.

We do not have a lack of advertising demand in the U.K. So these MAU growth initiatives are expected to result in positive returns shortly after implementation.

The auto enroll feature, rather than requiring users to opt in, is great. However, it sounds like it is only for new users, and not on the existing user base. Therefore, this will likely have very little impact in the near-term in the UK.

It also sounds like the new UK partner is on the smaller end, but maybe could benefit from the auto enroll change.

We are focused on increasing our MAU base by signing new partners. Our progress in our pipeline over Q4 is solid.

We're in discussions with multiple top 20 U.S. banks and several high upside fintechs, and we believe we will sign at least one of these major partners by the end of 2023.

It would be nice to sign one of the remaining large US banks, but I’m not sure that will happen until Chase and possibly others like BofA and Wells fully rollout the new user experience with new offer constructs and CDLX has quantifiable data to show the benefits of not only CDLX vs in-house or some affiliate program, but also from the new improvements (new ad server + new user experience + new offer constructs).

Given CDLX is still trying to sign fintechs, it would be nice to know if CDLX has plans to increase ARPU within the neobanks. While primary transactions are still in the traditional banks, there is pretty decent scale with CDLX’s existing neobanks, like Venmo and Credit Karma. While I essentially never transact with them, I have used Venmo offers when they are good enough, even just for 5% off next 3 gas transactions.

Therefore, while the vast majority or essentially all transactions won’t occur within these neobanks at this time, CDLX can still incentivize transactions + leverage more push notifications and other benefits that may be more restricted in the banks.

This could have a decent impact on overall CF given CDLX is about FCF positive + the size of these neobanks + given the operating leverage (where Dosh’s fixed costs are already a part of the overall cost structure).

However, focus should remain on the traditional banks given it will have the greatest impact, but I don’t won’t to lose sight of the potential and runway of the Dosh business.

9. Goal and Timing for MAUs on New Ad Server + New User Experience

On our last several calls, we have consistently talked about progress on 3 important product initiatives for our bank partners and advertisers. The new ad server, our new user experience and cloud migration. Each of these initiatives complements the other. And we are making great progress on all.

For the cloud, all of our major U.S. banks have data in AWS and 4 have systems in AWS. We expect nearly all of our major banking partners to move to the new ad server and user experience by the end of 2023.

I believe this is the first time hearing CDLX expects to have more major banks on the new user experience by the end of 2023, not just be on the new ad server (which is required for the new user experience).

There was a change in the presentation from having 100% of the MAUs by end of 2023, to now “nearly all” by the end of 2023.

At first, I thought that meant either BofA or Wells isn’t moving this year. If that was true, I was leaning towards Wells being the one taking longer, since I believe BofA is larger, which gets you closer to the “nearly all” language.

However, after speaking with others, I was told to not focus too much on the semantics between “100%” and “nearly all”.

Given the language in the call, it may be a function of trying to also fit into the expectation those banks moving to the new user experience as well.

Even if all the banks are not on the new ad server and rolling out the new experience this year, this is less of a concern, given Chase being the one on the new user experience (given it reduces the risk of leaving for Figg + one of CDLX’s largest partners so can have a large impact on its own + leads to enough scale for product-level offers).

Also, in a few years, will it matter if 100% of MAUs were on the new ad server and rolled out the new experience a quarter or so later than expected? Maybe depending on the macro environment, but I don’t think this will be something we discuss in the long term. As long as CDLX gets through the short-term, which I think they will given the Bridg dispute is behind them + CDLX has enough liquidity, then this isn’t the end of the world if this proves to be the case.

I think once Chase fully rolls out the new experience, as well as with new offer constructs, the other banks may accelerate their timelines or have an increase in the priority, especially if CDLX can provide data on the increase in benefits from the new ad server + new user experience + new offer constructs.

10. One Question on the Call

Hearing only one question on the call was strange. CDLX is covered by others like Chase and BofA, so I’m surprised someone from there wasn’t asking any questions (especially since they still updated their analysis after the call, but still posed their same concerns that they did not ask about…).

Possibly some impact from other earnings calls that occurred at the same time after hours, like Carvana, where some of these analysts are covering both. But I heard usually someone else then from the company would take their place for calls if multiple calls occurred at the same time.

There may also be some element of just less coverage or investors following the business, especially from the large price declines and entering micro-cap territory.

Just shocked me a little, since there were many things I was wondering about and wanted clarification on, but had to wait to hear from others who spoke to CDLX after the call.

(#174) 5.8.2023: Thoughts After Q1 2023 Earnings Call (Part 1)

I had quite a bit of notes and thoughts following the call last Thursday evening. However, I wanted to wait to send anything out until I had more time to discuss with others and think things through. This also got pushed back a little given I went to Omaha this weekend for the BRK meeting.

The following is only some of my notes. I plan to add the rest soon (likely tomorrow). I wanted to break it up into multiple parts, given the quantity of notes.

1. Cash Flow Positive Timing

CDLX changed their cash flow positive goal/guidance from “second half of 2023” to “as soon as possible”:

I didn’t think the Q3 CF goal would get pushed back, since CDLX just reiterated it when they announced the CFO transition. From what I am hearing, the change in expectation is from the recent change in the ad market and what CDLX is hearing from advertisers.

Obviously this is not what I wanted to hear, that it could now be later before turning CF positive.

However, this is much less of a concern after the Bridg dispute resolution, where there is now much more visibility into liquidity. I would be more concerned with this deferral of cash flow positive if we didn’t know the Bridg outcome, and we were wondering how tight CDLX was on liquidity.

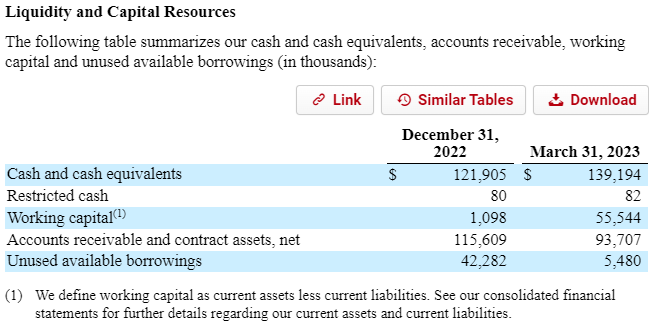

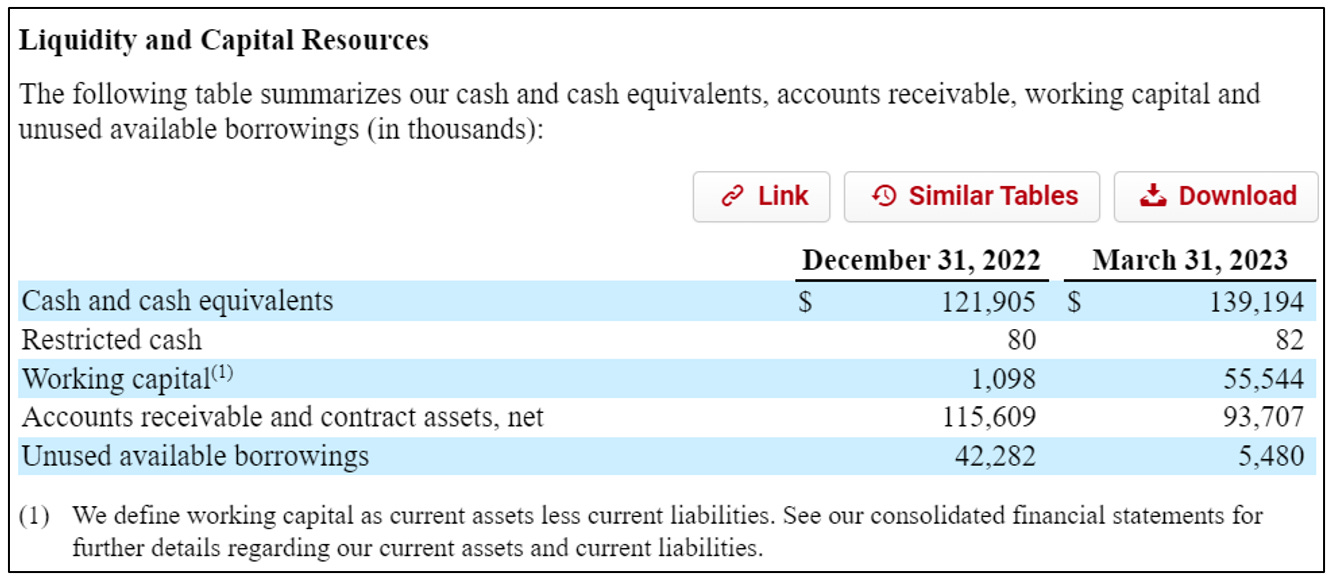

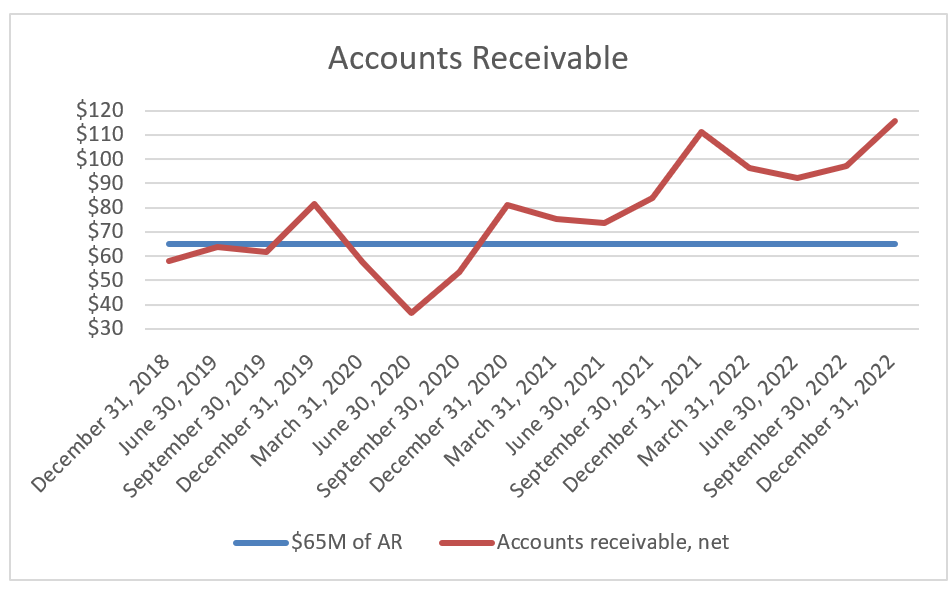

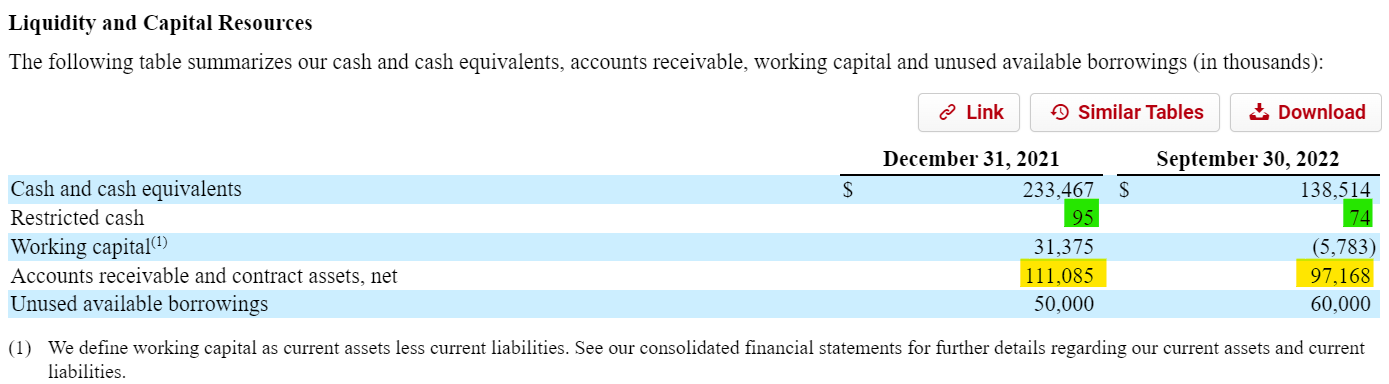

2. Liquidity Resources (Cash, Line of Credit, Accounts Receivable)

The following are the updated liquidity resources as of 3/31/2023:

CDLX’s cash position increased QoQ due to the $30M drawdown of the line of credit (LOC).

This drawdown is also partially to explain why the “unused available borrowings” decreased QoQ. The other reason for the decrease is from the decrease in accounts receivable which back the LOC and limit how much can be borrowed.

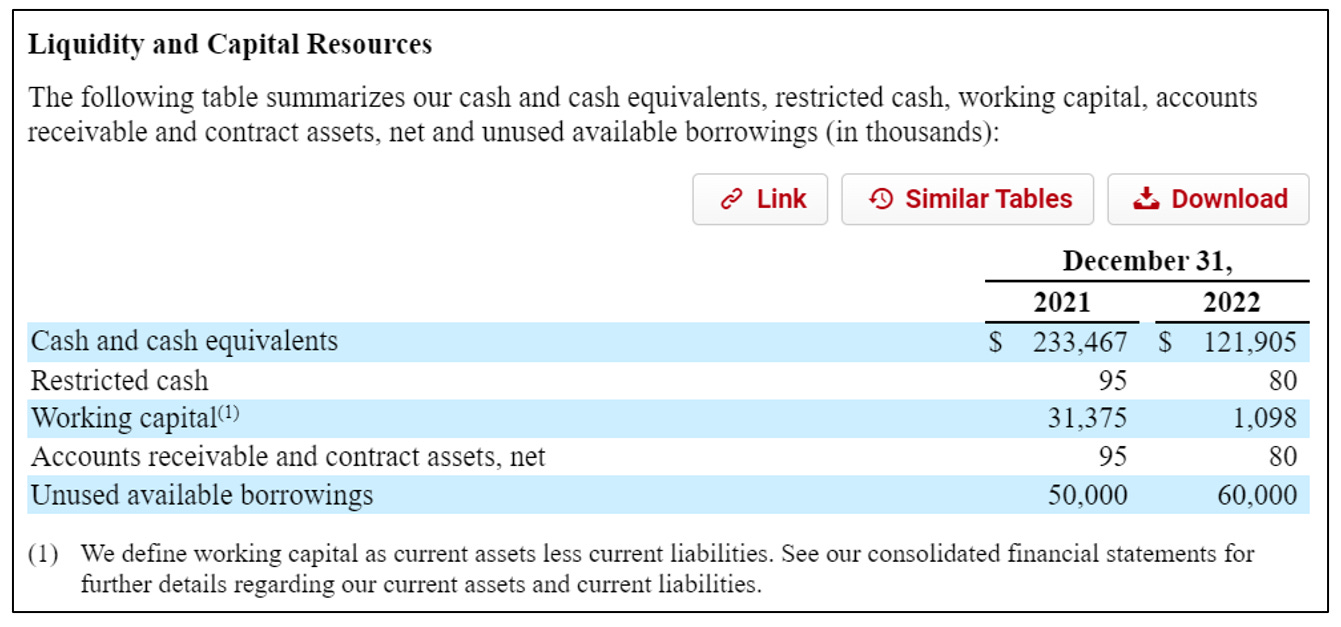

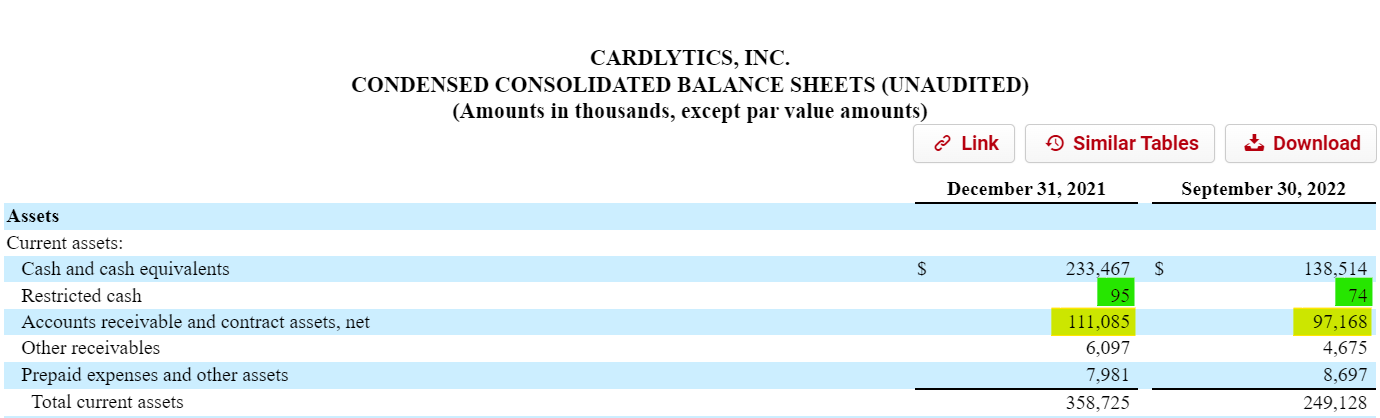

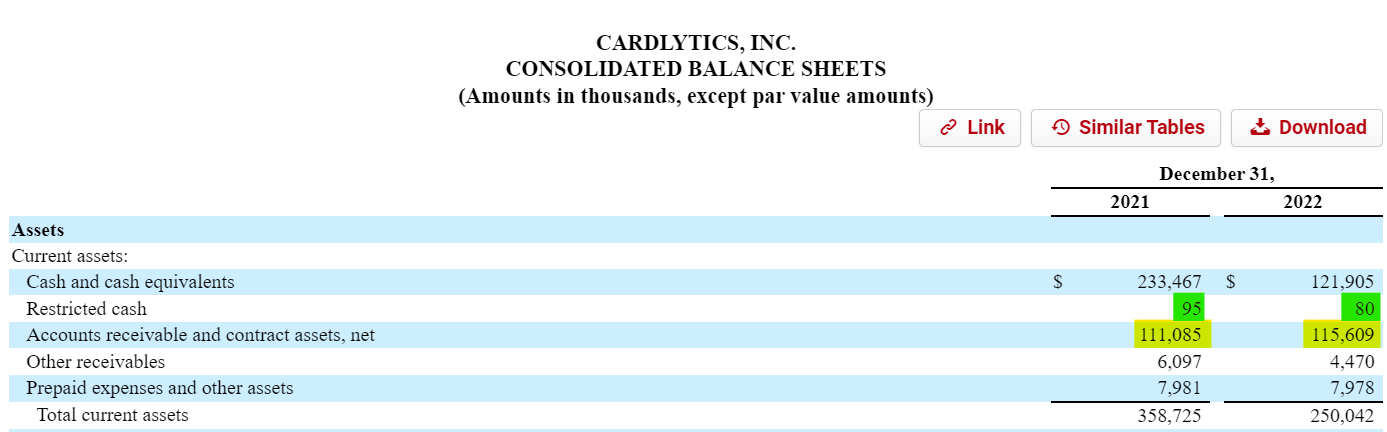

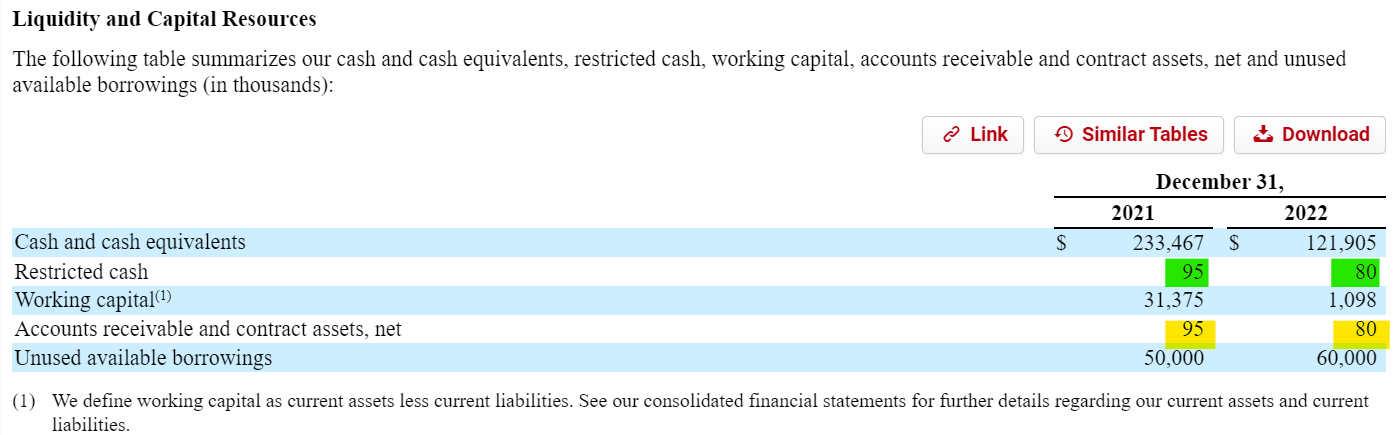

While we have 12/31/2022 above, I wanted to include the table from the 10-K, given some changes were made compared to the previously provided 12/31/2022 numbers.

For one, CDLX fixed their accounts receivable, which before was just equal to restricted cash and didn’t match the balance sheet. So now it is correct in the latest 10-Q.

CDLX also changed the “unused available borrowing”. In the 10-K it was $60M as of 12/31/2022, which was the max possible under the LOC. However, CDLX was limited to 50% of the US accounts receivable, which was less than $60M. Therefore, I believe CDLX also corrected this line to more accurately reflect what CDLX can actually draw down, and may also reflect other requirements. So seeing CDLX only had $5.5M of unused available borrowing wasn’t too surprising, given it was expected accounts receivable would come down, and given this is likely why CDLX only withdrew $30M and not more. But the remaining LOC capacity is also likely not a worry, given the Bridg outcome, and as seen next.

3. Updated Liquidity Numbers (Post Earnout and Q2-Q4 Burn)

Below are some quick liquidity numbers, based on the updated cash position, the known cash component of the Bridg earnout payment, and some estimates for the cash burn from operations.

$139.2M Q1 Cash Position

- $72.6M Bridg Earnout

- $13M Q2 Burn (mid-point of EBITDA guidance at -$8M, but then used $5M lower for FCF)

- $13M Q3 Burn (same as Q2 burn, vs FCF+ positive before)

- $13M Q4 Burn (same as Q2 burn, vs FCF+ positive before)

= $27.6M Estimated Ending Liquidity at 12/31/2023

To me this shows there are no near-term liquidity needs, and really shows the benefit of the Bridg earnout outcome, removing near-term liquidity fears. Therefore, CDLX should have some time to execute.

If CDLX needed some additional liquidity in the near term, such as from the ad market worsening, they could instead factor / securitize their accounts receivable, rather than use it as collateral for the line of credit. With $93.7M in accounts receivable, CDLX says they can only get access to $35.48M from it ($30M used + $5.48M unused), or only 38%. I have a feeling CDLX could get quite a bit more via factoring / securitizing, where a small percentage change is quite significant given the large amount of account receivable + in relation to the $20M-$30M ending liquidity position. I don’t think the current CFO will explore this option, so it will be a function of who comes in to replace him. Given CDLX’s partnerships with banks, this shouldn’t be too difficult, especially with accounts receivable that largely is composed of large national advertisers.

4. Chase and the New User Experience

One of our largest bank partners has rolled out the UI to more than 25% of its users.

25% of users currently on the new user experience is around the percentage I’ve heard other speculate, and seems to match my own small samples.

CDLX IR said Chase is rolling it out slower than CDLX expected, but their expectation is for 100% of Chase to be on the new user experience by the Q2 call.

I know others have been very concerned about the timing of the full rollout, but this has not bothered me, not even the slightest. I’m just happy Chase is actually rolling it out. US Bank has been on the new ad server for 2 years, and has only added pictures within the images, where Chase has done this and more, including adding images on the outside of offers and changed their intro offers format.

As I’ve said before, a phased rollout makes sense. I would have hated for Chase to rollout the new user experience to 100% of MAUs and find issues. This is why rolling out to even 25% to start is kind of surprising (compared to something much lower).

While it would be nice to have everyone on the new user experience today, it is also nice that that with a phased rollout CDLX can get more data on the impact of the new user experience (that can also be used to convince other banks to do the same, and for new banks to join CDLX).

While early, we have seen around a 50% increase in impressions on the rewards summary. We believe this is only the beginning.

As the new UI has rolled out, we've observed other engagement metrics on the new UI that are equally promising, and we intend to disclose some of these statistics when we have scaled data across more bank partners.

The 50% increase in impressions stood out. It is quite a large increase.

I don’t know for sure, but this could be from more time scrolling through the offers and seeing more offers, since it is now more enjoyable and insightful to look through the offers now since there are images on the outside of the offers. There could also be a benefit from the new categorization, which I believe could increase the frequency of openings (such as discussed in update #172).

This could get interesting if CDLX started charging for impressions, which I heard was possibly one of the new monetization models Karim was exploring, and would then make sense why this was an engagement stat that was shared.

In general, you would expect higher impressions to increase the odds of users finding relevant and attractive offers, and increasing redemptions and ARPU. I would very much like to know the difference in redemptions and ARPU for these users before concluding that is occurring. It doesn’t matter if impressions are higher if it doesn’t translate to higher ARPU.

5. New Offer Constructs and Timing

Spend Stretch Offers

We expect to launch an alpha version in Q2 of the spend stretch offers that we discussed on the prior call. As a reminder, spend stretch allows advertisers to incentivize a set of customers spending in a certain range to increase their spending on the next visit.

For example, customers who spend $20 on average could receive a $5 cash discount if they spend $40 or more.

Good to hear new offer constructs like spend-stretch offers will be rolled out in Q2.

There may also be a benefit from this new offer construct being more similar, or even the same, as AmEx offers.

I don’t know how many, if any, advertisers are directly involved with placing offers in AmEx, rather than just AmEx placing offers on their behalf and funding them, but there could be some benefit from the similarity aspect:

For one, if advertisers are involved with these AmEx offers, or have even just seen them work with success, having a similar offer construct on CDLX could help increase the odds of them placing offers with CDLX.

There may also be a small increase in probability of signing AmEx, if CDLX can give them the offer construct they are used to placing.

Multi-Tier Offers

We also expect to launch an alpha version of multi-tier offers in Q2. These offers allow flexibility for advertisers to provide variable incentives based on their objectives. The steering structure also gives customers more choice.

For example, a travel client can reward 10% on all stays in Los Angeles and 5% on all other states in the U.S. Our subscription provider could reward 10% back on annual subscriptions and 5% back on all other purchases.

CDLX actually placed this offer in US Bank (who is on the new ad server) back in August 2022:

Spend Stretch vs Multi-Tier

We have already seen some examples / tests of these new offer constructs. However, I am not positive which definition they fall under at this time.

In a past conference, Karim used the United Airlines example where you earn 5% when you spend $50 or more, but earn 10% when you purchase an Economy Plus ticket. Before this was defined as the spend stretch offer, but now it almost feels like it is the multi-tear offer given the different objectives.

There have also been tests in Dosh, such as with Panera, where the more you spend, the more you save. I feel like this is a spend stretch offer.

: Chase Launches the New User Experience, Austin Swanson, Swany407")

Product-Level Offers

I did hear that CDLX plans to start placing some product-level offers in the second half of 2023 with one of the large bank partners (which I assume is Chase, given they are already on the new ad server and new user experience).

I was pleased to hear this, given I was a little nervous from not hearing an update on the call.

6. New Targeting

Here are 2 new targeting features we released in our Ads Manager.

First, share of wallet or functionality that allows advertisers to target audiences who shop and spend at competitive brands. A great example is a large restaurant customer that wants to increase breakfast traffic could target only customers of breakfast brands.

Second, mean max targeting or the ability to let advertisers target based on minimum or maximum amounts of spend during the same period. This gives advertisers a tool to drive elevated spend from the current customers.

This surprised me a little at first, where I thought at least wallet share targeting was already a part of CDLX and a key feature of the platform.

However, what I missed the first time while listening to the call was this was added to the new ads manager, which has the self-service component for advertisers. (As a reminder, as even Karim has mentioned in the past, there were many aspects that may have been less automated or more manually done by CDLX, so this could be one step in that direction.)

Closing

I will be adding the rest of my notes soon, such as regarding the UK Bank, MAUs on the new ad server, and more.

Q1 2023 Earnings: Notes and Thoughts Before the Call

(#173) 5.4.2023: Final Thoughts Before Today's Earnings Call

Cardlytics releases their Q1 financial results and has their earnings call after market close today.

Below are most of the items I am looking forward to hearing/reading about within the new 10-Q and hear on the call (or get clarification after today’s call). I am using this somewhat as a checklist, to not forget anything to check up on.

Bridg Earnout

Timing of the Bridg earnout payment (if not already completed)

Details on the dispute (such as was it regarding how joint contracts were allocated?)

Details on the second earnout (and whether it going to zero was due to the change in method caused by the dispute, and related to joint contracts like SBUX)

Chase on the new ad server and rolling out the new user experience

This has never been publicly announced yet, so today is likely the first time

I’m not sure if CDLX will mention them by name. CDLX usually will not single out a bank.

Could lead to some favorable reactions, given it confirms Chase was the 1st large bank to move to the new ad server + decreases likelihood of Chase leaving anytime soon. But again, how many do not already know about this?

Early stats and engagement (activations, first time users, click-out rates, redemptions)

Why not fully rolled out to all users yet

Timing of product-level offers and new offer constructs

Also haven’t heard anything regarding the self-service for banks (“Engage”) recently

100% MAU Goal

Could have a surprise with 100% of MAUs on the new ad server, ahead of schedule

In the 22Q3 call, “We are also rapidly migrating our bank partners to the cloud and made significant progress in the quarter. We believe we can migrate nearly all of our banks by Q1 of next year, which places us well ahead of our Q3 2023 goal.”

I think Wells and BofA will want to get to the new ad server and rollout the new user experience quickly with Chase now live with it. So maybe Wells and BofA are already on the new ad server.

Current Financials

Cash position (such as after Q1 burn + drawdown of LOC on March 14th + if collected any accounts receivable)

Future Financials and Q2 / Q3 / FY Guidance

More than anything, I just want to have an idea what Q2 Burn will be (based on assuming an amount larger than their EBITDA range)

Also want to see that CDLX is maintaining their expectation of being FCF+ by Q3

Would be nice to see a full year guidance as well

New Banks

Any new banks added, or any change in commentary related to partnering with new banks

During the 22Q3 call, “We are in discussions with multiple top 20 U.S. banks and several high upside fintechs. While these conversations are early, our pipeline to increase MAUs over the next 2 years is strong.” Karim has also mentioned partnering with international banks.

There was also a recent hiring for an Integration Consultant, but that could be related to moving banks to the new ad server, but still possible it is related to a new bank (since I believe this team handles both)

PacWest and LOC

Impact if PacWest goes under

Remaining available on LOC (will have to take into account updated accounts receivable, and I would like to know more about how the minimum adjusted cash works)

If there are any new LOC amendments

Investor Day

There has been mention that CDLX would hold an investor day in May, so I am curious if this will be mentioned today

2025 Senior Convertible Notes

I am not sure CDLX will address this, but it could be asked about in the questions on the call (I am not worried about these converts, but others are, so removing this concern could be beneficial to the stock price)

Reporting Corrections

There were quite a few errors in the Q4 information released, so it would be nice to see all of these fixed (quarterly vs annual MAUs were flipped, liquidity resources reported wrong, inconsistent change in ARPU calculation, material cash requirements timing was off, etc.)

RSUs

Would like to update my assumptions based on new unvested RSUs

Karim and Nick Lynton (Chief Legal & Privacy Officer) got 200K and 100K RSUs respectively. I also would like to know more details regarding those 200K and 100K RSUs. Makes sense if tied to the Bridg resolution, since it seems it was only those two who received RSUs.

New CFO

Heard CDLX may have already hired someone that could become CFO. Not sure if CDLX will address this.

Dosh

Partners: Looks like Dosh signed at least one new partner, “h.way”, possibly as of May 3rd. There could be others.

App: Dosh recently updated their UI. Not sure if CDLX would discuss this at all, such as where tested items have worked well and could later be seen in the banks.

Bridg and RMNs

Would be nice to hear more about Bridg and their shift to Retail Media Networks. This may have to wait until an investor day. Not sure if they will ever mention any clients by name.

Entertainment

Would like to know if CDLX still plans to add Entertainment offers on the new user experience

Still have not had an update on the AmEx trial of Entertainment subscription, which may have just recently ended

I know they are releasing an updated Entertainment app soon, so some focus must still be on it

$100M Shelf

I don’t expect CDLX to raise at these prices, given both Karim’s past comments + no real need at this immediate time. However, some have been worried given the recently filed $100M shelf. But we know this was more a formality now that they are <$700M market cap and loose their well-known seasoned issuer (WKSI) status. May be beneficial to CDLX and their stock price if CDLX addressed this, but that seems less likely.

I put together this list just this morning, so there are likely other important information I am missing, but I will address after the call.

Given the Bridg dispute is done, there should be a window where CDLX insiders can buy after the call. It would be great to see even just a little insider buying.

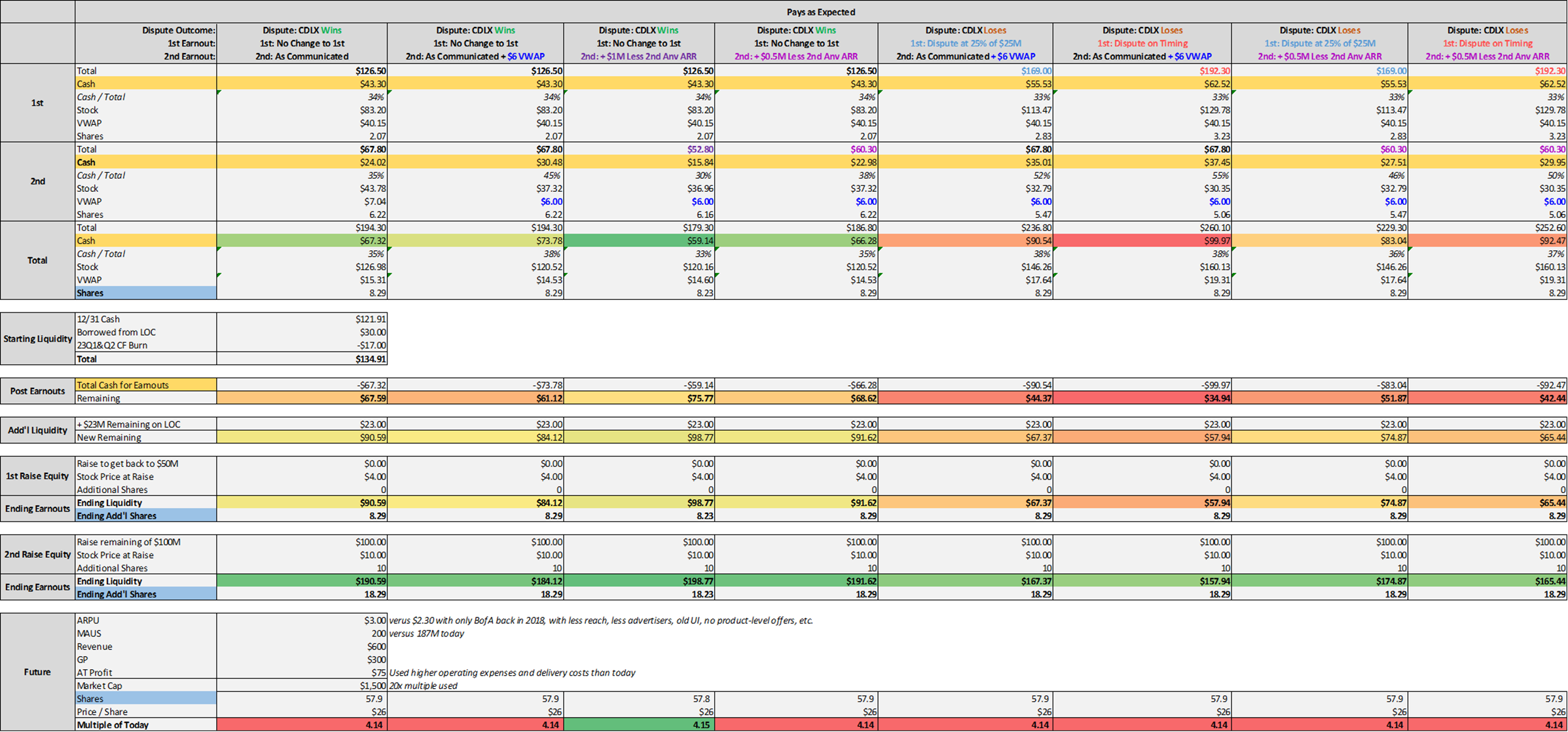

(#171) 5.1.2023: First Thoughts on the Bridg Dispute Outcome

Cardlytics Announces Update to Bridg Earnout Payments

Today, May 1st, 2023, CDLX announced:

An Independent Accountant determined the First Anniversary ARR to be $23.2 million.

Based on the Independent Accountant’s determination and the terms of the merger agreement, the First Anniversary Payment Amount would be $208.1 million, inclusive of fees and transaction bonuses and accounting for all true-ups and credits.

Cardlytics anticipates the Second Anniversary Payment Amount due under the merger agreement to be $0, inclusive of brokerage fees and transaction bonuses and accounting for all true-ups and credits.

In sum, the total cash anticipated for both earnouts, inclusive of brokerage fees and transaction bonuses and accounting for all true-ups and credits, is $72.6 million.

Cardlytics anticipates the remaining consideration for both earnouts will be paid with 3.4 million shares of Cardlytics common stock, which significantly decreases investor dilution as compared to Cardlytics’ previous publicly disclosed estimates.

The issuance of these shares will result in dilution of approximately 10.0% to the ownership interests of existing stockholders, based on the number of shares of common stock outstanding as of February 28, 2022.

“We are pleased to reach a conclusion in the Independent Accountant proceeding that gives us clear visibility into the total amount of both earnout payments, which are collectively in line with the expectations we set out on our most recent earnings call. I am also delighted that the outcome will reduce shareholder dilution significantly from our previous estimates and we expect that it will eliminate any additional cash outflow stemming from the second anniversary earnout payment obligation,” said Karim Temsamani, Chief Executive Officer.

First Earnout versus Expectations / Fears

An Independent Accountant determined the First Anniversary ARR to be $23.2 million.

Based on the Independent Accountant’s determination and the terms of the merger agreement, the First Anniversary Payment Amount would be $208.1 million, inclusive of fees and transaction bonuses and accounting for all true-ups and credits.

This $208.1M compares to $126.4M expected by CDLX, or $81.7M more. This large difference is from the large increase in ARR (I will discuss this more below), where the first earnout was a function of 20 x (ARR - $12.5M). Therefore, even a small increases in the ARR could lead to large increases in the first earnout.

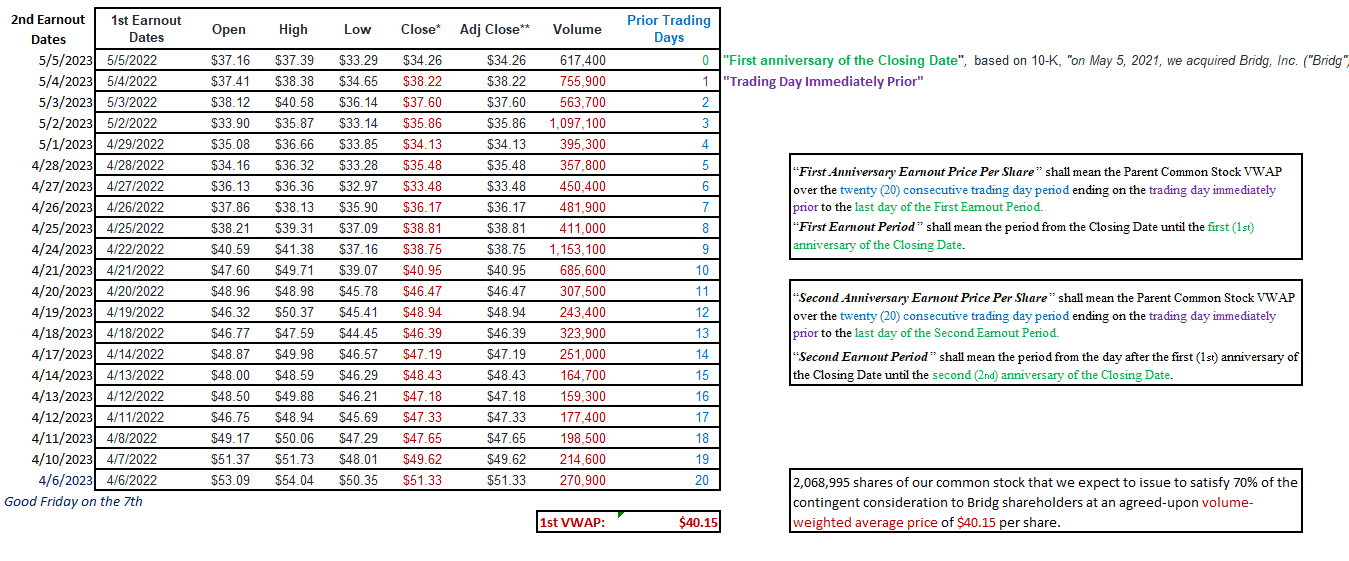

One benefit CDLX had was that the dispute was on the first earnout payment, which had a $40.15 VWAP that applied to approximately 70% of the payment. Therefore, the increase in the cash component was not near as much.

Cash versus Expectations / Fears

In sum, the total cash anticipated for both earnouts, inclusive of brokerage fees and transaction bonuses and accounting for all true-ups and credits, is $72.6 million.

The $72.6M in cash for both earnouts compares to CDLX’s expectations of $67.3M ($43.3M for the 1st earnout + $24.0M for the 2nd), or only $5.3M / 7.9% more cash than expected.

While the actual payment is higher than what CDLX expected, this total cash payment of $72.6M is significantly lower than the amount investors feared from the dispute, as well as from the low stock price impacting the second earnout (where a lower stock price = lower stock component = higher cash component).

I had some estimates of ~$115M in cash that could be owed depending on the dispute outcome and second VWAP, so this actual outcome is much better.

Also, with this low level of cash, I wasn’t expecting this little of dilution.

Dilution versus Expectations / Fears

Cardlytics anticipates the remaining consideration for both earnouts will be paid with 3.4 million shares of Cardlytics common stock, which significantly decreases investor dilution as compared to Cardlytics’ previous publicly disclosed estimates.

The issuance of these shares will result in dilution of approximately 10.0% to the ownership interests of existing stockholders, based on the number of shares of common stock outstanding as of February 28, 2022.

The 3.4M shares for the first earnout is higher than the 2.07M CDLX was expecting.

But 3.4M of total shares compares to 6.7M-8.3M some where expecting, so there is much less dilution in total than expected. This higher expectation was based on the 19.9% dilution cap that could have come into play (where the range is from it depending on how the cap was applied).

This outcome of 3.4M shares in total for both earnouts is also dramatically lower compared to the dilution feared by those who were not aware of the dilution cap (they were worried about a continually decreasing stock price leading to more shares issued, which could lead to a lower stock price, and so on…so they feared unlimited / infinite dilution…but I think many later became aware of the dilution cap).

This lower total dilution comes from the 100% weight to the 1st earnout with a $40.15 VWAP. The VWAP on the second earnout would have been much lower. Given the second earnout is $0, that lower VWAP does not come into play.

Second Earnout $0

“Additionally, because of the Independent Accountant’s determination, Cardlytics anticipates the Second Anniversary Payment Amount due under the merger agreement to be $0”

One reason the second earnout could be $0 is from the second earnout being based on the increase in ARR for second anniversary customers only. Therefore, given the first ARR increased, there may now be no increase in ARR for these second anniversary clients, leading to the $0 for the second earnout. This is very good, given the significantly lower VWAP on the second earnout that no longer comes into play (which is why there is so much less dilution than expected).

There were also mentions before where Bridg was disputing the allocation of a large joint CDLX / Bridg contract (likely the $25M two-year contract), where Bridg wanted more of that contract allocated to them.

If that is true, it could be that this allocation method (that was disputed for and ruled in favor of Bridg) led to this higher ARR and first earnout payment.

However, given the change to Bridg’s method, it could have also changed other joint contracts.

Given Starbucks was both a CDLX and Bridg client, CDLX may have actually benefited from SBUX leaving during the dispute under this new method, since it likely contributed to this $0 second earnout.

(There may also be some insights from the fact it is $0 for the second earnout, and not some lower number like $4.321M vs the $67.8M that was expected. There was likely a very large decrease in the ARR for second anniversary customers [such as from SBUX leaving] that lead to being below the first ARR. Therefore, with no increase in the total ARR for these second anniversary customers, the second earnout is zero).

This is also why the odds of Bridg disputing the second earnout are likely very low. The judgement was ruled in favor of Bridg, where this possible change in method of allocating joint contracts is likely what also led to the decrease to $0 for the second earnout. Not sure how Bridg can dispute exactly what they wanted and won. I think disputing your own dispute would be a first.

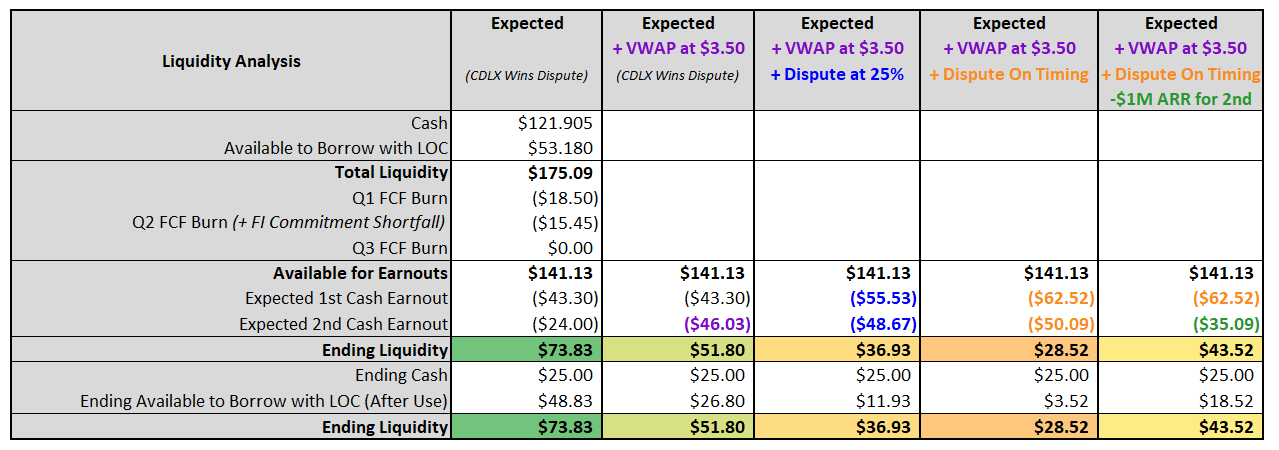

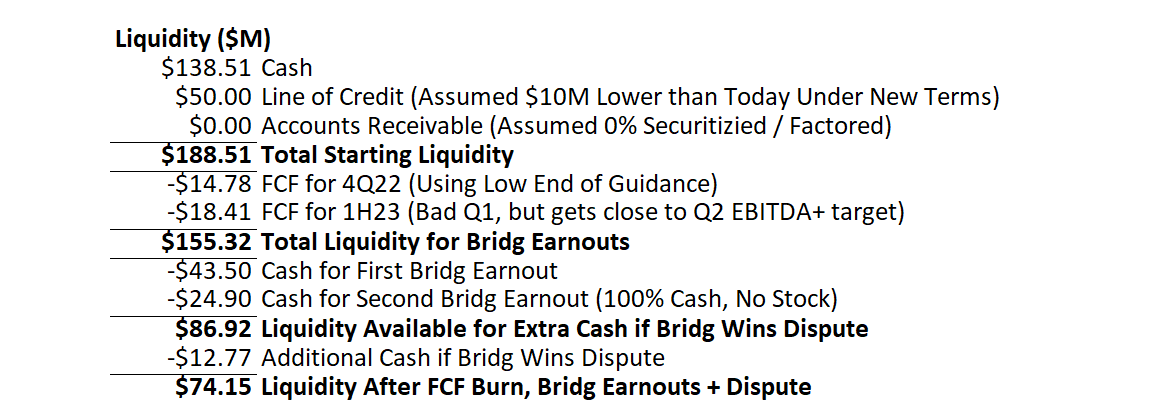

New Liquidity Position

Below is a quick CDLX liquidity analysis that factors in this Bridg outcome:

$121.9M cash at 12/31/2022

+ $30M drawdown of LOC

- $20M FCF burn for Q1 and Q2 (then FCF+ in Q3)

- $72.6M cash for both Bridg earnouts

= $59.3M ending liquidity

Again, the ending liquidity amount above is after Q2 and the associated burn. And given CDLX still expects to be FCF positive in Q3, CDLX is positioned well.

The above also ignores:

Remaining liquidity available under the $60M LOC

Possibility of lower cash flow burn in Q1 and Q2 (from better than-expected results)

Possibility of CDLX collecting some of their $115.6M in accounts receivable (leading to higher cash flow)

Therefore, CDLX has plenty of liquidity to handle both Bridg earnout payments (and accomplished with less dilution than expected).

So it doesn’t look like CDLX will be going bankrupt from the Bridg earnouts (as some have feared).

2025 Convertible Senior Notes

Some may now shift their focus / fear to the $230M of 2025 convertible senior notes, but CDLX has over 2 years to worry about them.

Given CDLX is going to be FCF+ in Q3 of this year, I believe CDLX won’t have too difficult of a time getting new debt to refinance these 2025 converts.

Or CDLX could issue stock to cover. While at today’s prices this would lead to a lot of dilution, it would still mean CDLX doesn’t go to zero due to the converts. But there is no reason for CDLX to do that at this time. CDLX will instead continue improving and growing the business, which will likely lead to a higher stock price, decreasing the dilution that could occur.

Underappreciated Secondary Benefit

CDLX CEO, Karim Temsamani, ended his statement by saying,

“We are excited to move past this short-term issue while we continue to focus on our strategic priorities.”

This may be an underappreciated aspect of resolving the dispute.

Karim and others have likely been spending a large amount of their time dealing with this dispute. With the dispute now behind them, they can have more time + focus for improving and growing the business.

Closing Thoughts on the Bridg Outcome

Overall, this is a very good outcome for CDLX, with significantly less cash and dilution than what was possible / feared.

And given the outcome has led to much less dilution for CDLX with only a little bit more cash, one could say the dispute ended up working in CDLX’s favor.

These are only my first thoughts on the news. I will add more information as I hear and learn more, such as following the upcoming earnings call.

(#170)

The following was saved off here (removed within the notes to save space)

(#170) 4.27.2023: Updated VWAP Projections (5 Days Remaining of 20) + Additional Bridg Earnout Payment Possibility

(#166 - #169)

The following were saved off here (removed within the notes to save space)

(#169) 4.25.2023: Updated VWAP Projections (7 Days Remaining of 20)

(#168) 4.24.2023: Follow-up Thoughts on the Timing of Q1 Earnings + Announcing the Bridg Resolution

(#167) 4.23.2023: Thoughts on the Timing of Q1 Earnings + Announcing the Bridg Resolution

(#166) 4.22.2023: Updated VWAP Projections (9 Days Remaining of 20)

(#164 - #165)

The following were saved off here (removed within the notes to save space)

(#165) 4.18.2023: Updated VWAP Projections (12 Days Remaining of 20)

(#164) 4.17.2023: Current VWAP for 2nd Bridg Earnout Payment + VWAP (Stock Prices and Volume) Projections

(#163)

The following was saved off here (removed within the notes to save space)

(#163) 4.12.2023: Potential Stock Price After the Bridg Resolution

(#161) 4.7.2023: Interpreting the Possible Timings of Announcements

Bridg Resolution + Q1 Earnings

While this is something I would rather not give too much weight to, especially given all the possible scenarios, I cannot help but consider what the timing of the announcement may mean related to the Bridg announcement.

Or more specifically, if we don’t hear something on a given day, whether that is good or bad.

For instance, if CDLX already knows the outcome the dispute from the judgement of the independent accountant:

Announcing Monday

If CDLX already knows the judgment, I feel it is much better for CDLX not to announce until Monday morning, before opening. This could lead to a better stock price reaction, similar to the announcement related to updated guidance. This of course assumes a favorable resolution.

Announcing Today (Friday)

Compare that instead to CDLX also already knowing the judgement of the dispute, but announcing it sometime today, possibly 4pm CST. I feel that is a little sketchy, given the holiday, almost as if they are trying to hope less people see the news (especially given it is a holiday weekend), and react less on Monday.

However, maybe the resolution is favorable to CDLX, so announcing early / today allows for more time for others to see it and understand it, and react better on Monday. Also gives more time for word to spread and for others to discuss. Given the VWAP is based on the 20 trading days, there isn’t too much time to waste with getting the stock price up, so leveraging the weekend isn’t the worst idea.

So it may be a good sign nothing is announced today, but it is too hard to read too much into it, since it all depends on the actual results.

It is also possible CDLX does not already know the results of the dispute, so these thoughts mean nothing today. But if we heard nothing Monday - Friday morning next week, I will probably have similar thoughts during the day Friday, and wondering if something will be announced after hours.

Again, there is only 20 trading days for the Bridg VWAP, and I believe that started with April 6th, so CDLX is incentivized to get the stock up as much as possible and as soon as possible. However, they likely have no control on when they learn about the judgement of the independent accountant, but they may have some control on when they announce it.

It could also happen that CDLX hears the judgement, then appeals it. If that occurs, I’m guessing we don’t hear about that until the May earnings. And given the VWAP window, maybe then CDLX pushes back the earnings date (maybe later than May 2nd compared to last year).

Related, I think if CDLX announces earnings will be earlier this year (say even before May 1st), that is a positive, as it indicates they are trying to get out good results + announcements earlier to help with the stock price for the VWAP.

On the opposite side, if CDLX hears the judgement and it is favorable to CDLX, but Bridg disputes it, I think CDLX could announce the favorable judgment, but maybe would wait until earnings to say Bridg is appealing it. Again, CDLX needs to do what they can to help the stock price for the VWAP (within what is allowed / possible).

Chase Rolling out the New User Experience

CDLX has yet to publicly announce that Chase is the large bank that moved to the new ad server and is rolling out the new user experience.

I think most know this, but there could still be some positive reaction on the stock if CDLX announces this.

Give we have haven’t heard an announcement yet, despite knowing about this for a while, and users such as in my household have the new user experience, I think CDLX / Chase could be waiting until all users have the new user experience.

In the past, I have seen Chase push through updates on Friday and Saturday nights, so maybe this is the weekend the remaining users get the update, and an announcement follows.

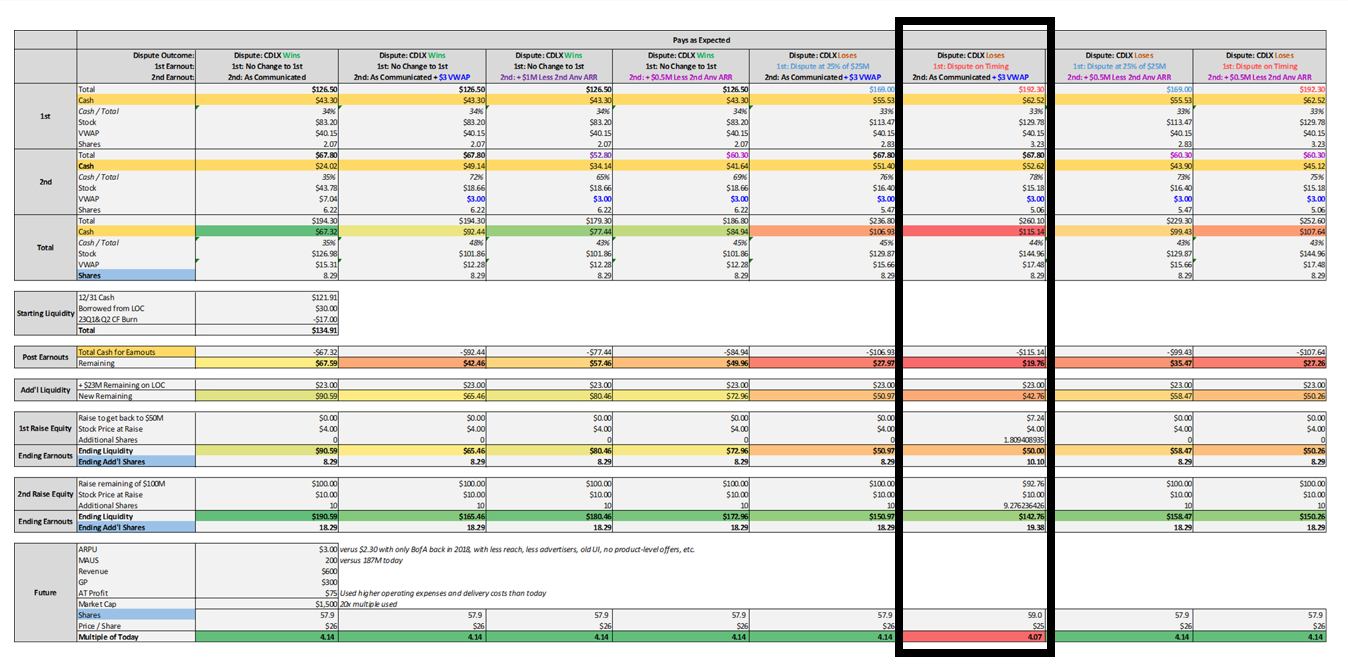

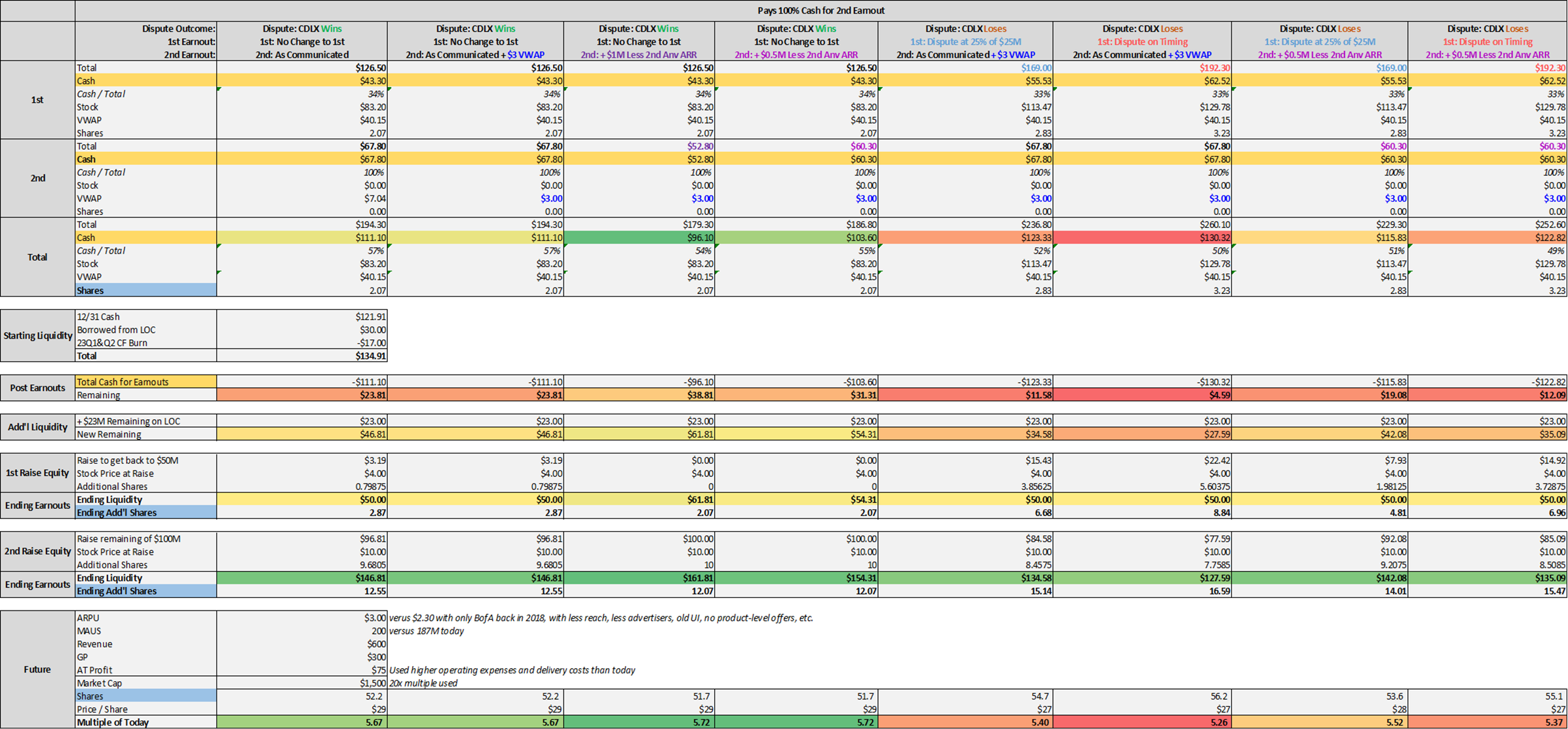

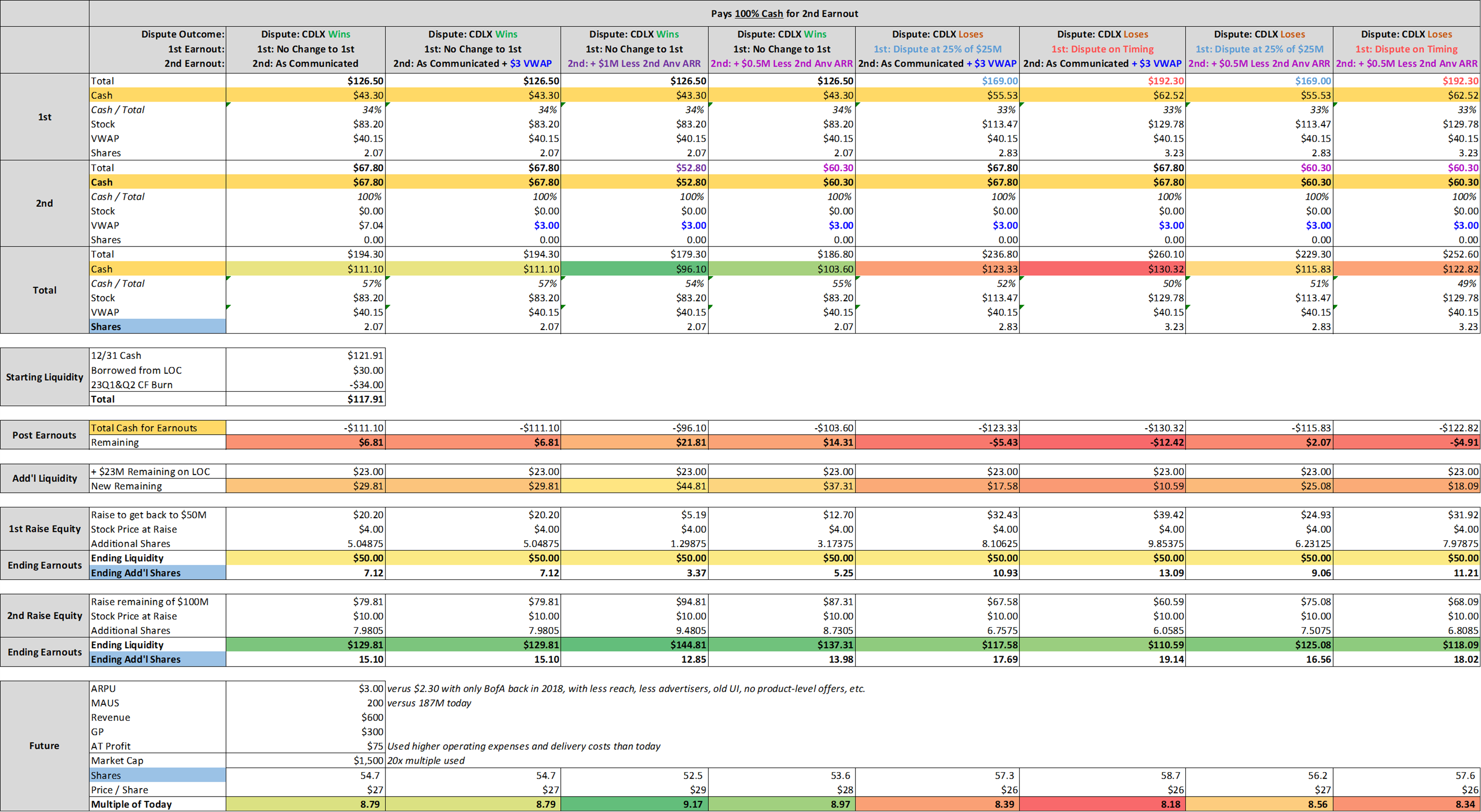

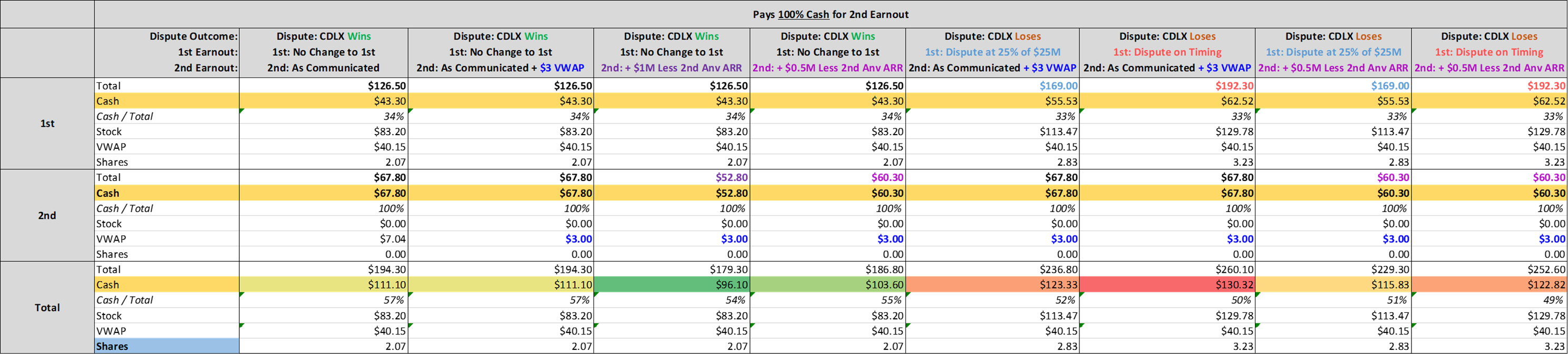

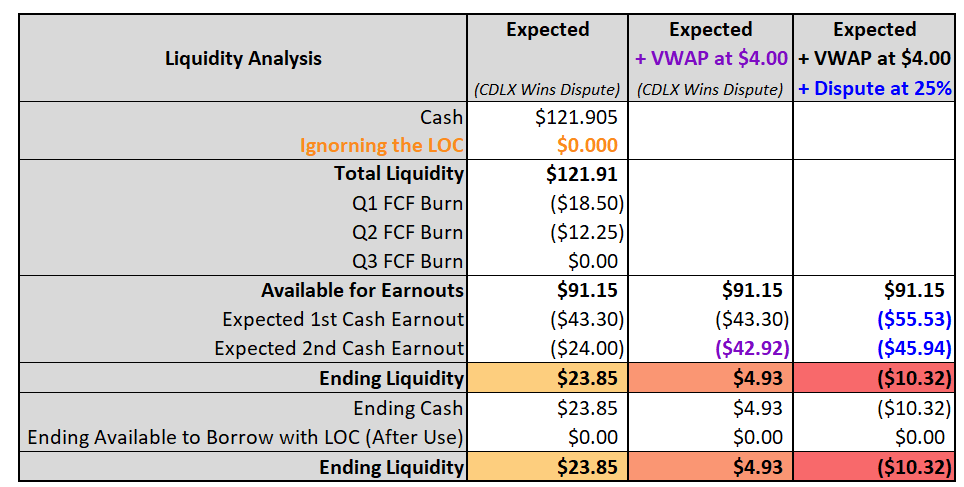

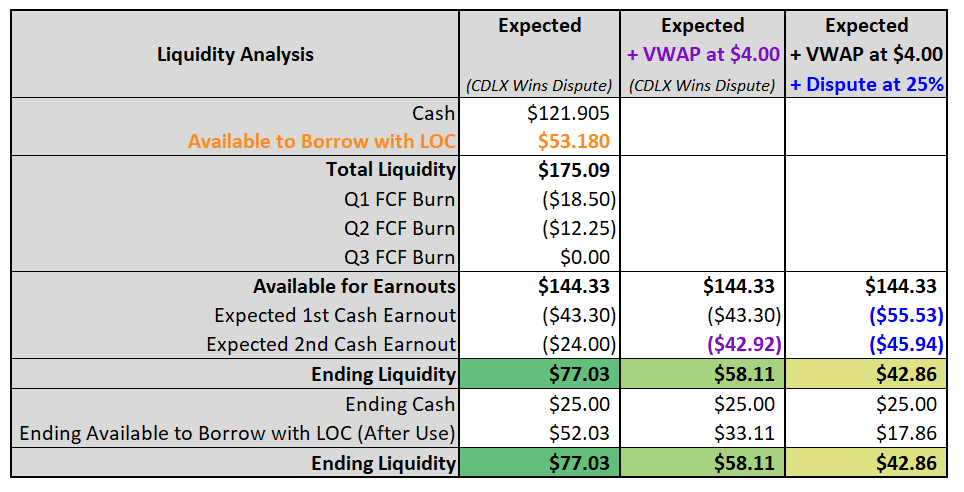

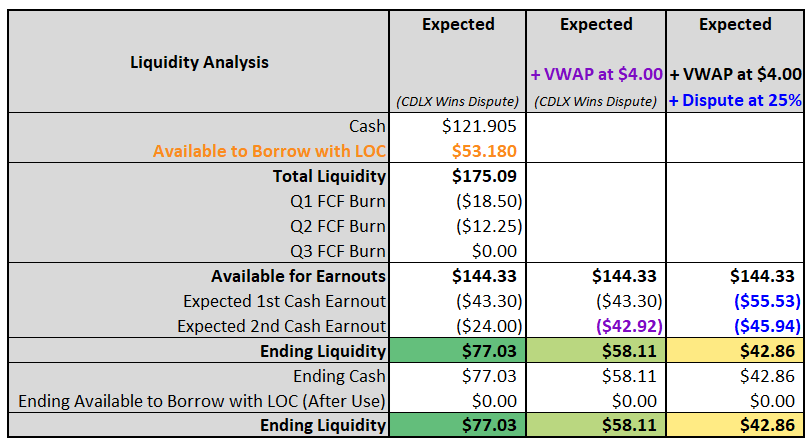

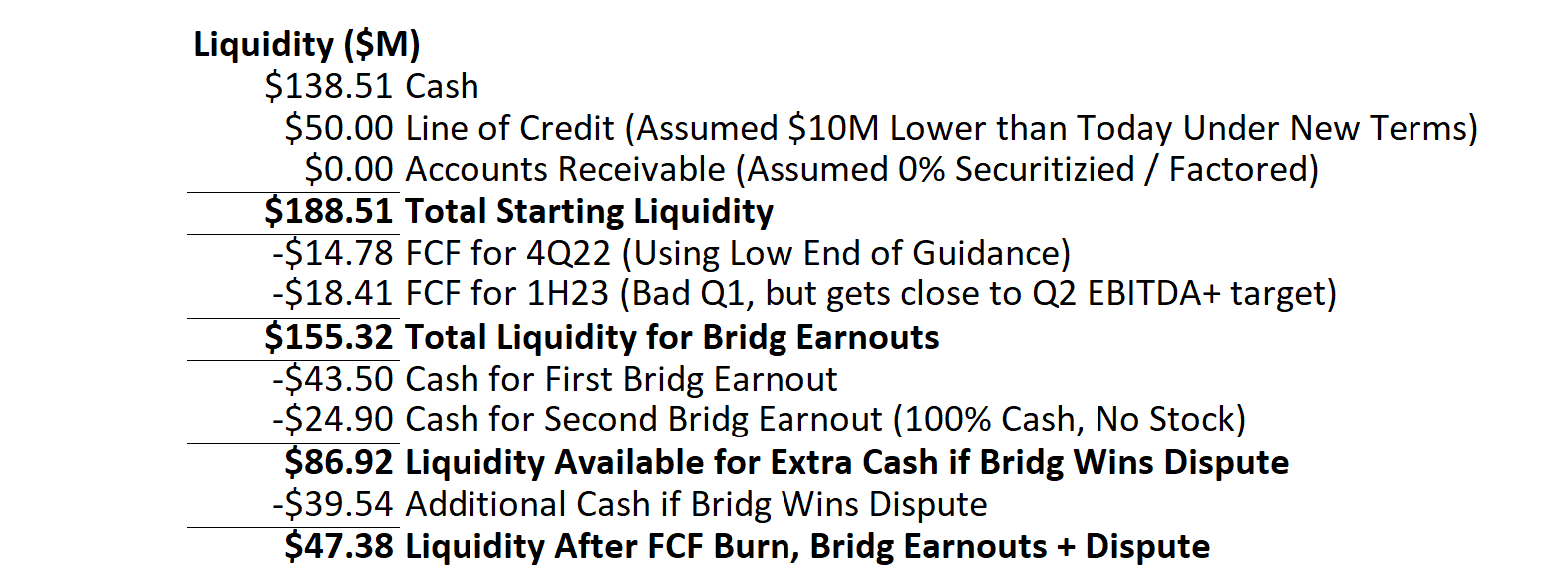

(#160) 4.5.2023: 2025 Convertible Senior Notes + Updated Liquidity Analysis / Share Count / Future Value (with 100% cash for 2nd earnout)

Projection 5: 100% Cash for 2nd Earnout

I wanted to provide another projection (#5) in addition to the 4 provided yesterday (below).

The following is with CDLX paying 100% cash for the 2nd Bridg earnout payment.

I have discussed this possibility in the past, and have used it in my prior analysis as well. The reason CDLX would do this is from having plenty of liquidity to do so, leading to not using stock at the lower prices today, leading to less dilution.

If CDLX wins the dispute, and pays the 1st earnout as expected (the first 4 columns of results) then Chase has plenty of liquidity to do 100% cash for the 2nd (as seen in the row of liquidity following both Bridg earnouts).

This is even more possible this week vs the past, given the updated guidance, leading to less cash burn, so more liquidity. And as seen in column 3 and 4 of results, if the 2nd earnout comes in lower than expected (which is possible, and could be announced soon), it leads to even less cash needed.

If you compare these results to those provided yesterday, it leads to less ending liquidity (given using more cash for the earnouts), but less dilution (where CDLX would not likely need to raise the additional $100M that I assume here, but I keep it in for conservatism).

A few notes:

CDLX’s liquidity before the earnout payments is likely higher than 12/31/2022 cash of $121.9M (which some are assuming), given CDLX already drew down $30M from their line of credit, which is likely more than cash burn in Q1 and Q2 (especially given the updated guidance yesterday)

I’ve ignored the possibility of accounts receivable coming down in Q1, leading to more cash (AR was quite high in Q4, and we sometimes see this come back down in Q1)

There may also be more available to draw down on the $60M LOC (but note, this is a function of 50% of US accounts receivable, so if AR goes down, there would be less to draw down on the LOC, but it also means CDLX likely has more cash from the AR, which is likely more beneficial than only 50% with the LOC)

I also ignore some timing benefits related to when the Bridg earnouts are paid (I have 100% of Q2 burn occurring before the 2nd earnout occurs, when in reality that will likely occur before the end of Q2, meaning there is more liquidity immediately following the Bridg earnouts).

2025 Senior Convertible Notes (over 2 years away)

Some may look at the ending liquidity and think, “that is not enough for the convertible notes!”.

The liquidity analysis above is based on today and the very near term. The coverts are not due until September 2025, or over 2 years from now.